ICSI - WIRC FOCUS

Vol. XXX • No. 07 • July - Aug 2013

Chairman’s Blog

My Dear Professional Friends,

My Dear Professional Friends,

I sincerely hope that the Digital FOCUS is welcomed by you all, and you have enjoyed the new Avtaar of FOCUS. I have received compliments from many members for this Green Initiative of ICSI-WIRC.

In last two months various programs were conducted by ICSI-WIRC and Chapters and all of them were attended by students/members in large number.

On 5th July 2013, ICSI-WIRC inked a MOU at Company Secretaries’ Conference at Pune for launching “Talentick” which is a Placement Initiative of ICSI-WIRC in collaboration with Camplace Pvt. Ltd. “Talentick” is a platform through which students / members can have interface with prospective trainers/employers. The ICSI-WIRC has also signed two MOUs with Vikas College, Vikhroli, Mumbai and N. M. College, Ville Parle, Mumbai on 15th July 2013 and 20th July 2013 respectively for conducting Class Room Teaching Centers. Similar MOU with R. A. Poddar College at Matunga, Mumbai is being formalized. Our President CS S.N. Ananthasubramanian was invited by R. A. Poddar College on 13th July 2013 to deliver a talk on “Career as Company Secretary” which was attended by large number of students.

The biggest event of the ICSI-WIRC – Annual Regional Conference 2013 – at Starz Club, Ahmedabad held on 3rd and 4th August 2013 was a huge success despite heavy rain in the city. The Conference also coincided with the 40th Foundation Day of Ahmedabad Chapter. The State level Students’ Conference at Raipur, Chhatisgarh on 11th August 2013 on theme “Class Room to Board Room” was successfully held to celebrate the 15th Foundation Day of Raipur Chapter. The State Conference at Bhayendar Chapter held on 17th August 2013 on the same theme was also attended by large number of students. I was fortunate to have attended all the above programs. CS S.N. Ananthasubramanian attended the Annual Regional Conference and Bhayendar Conference. CS M. S. Sahoo, Secretary, ICSI graced the Conference at Raipur.

The ICSI-WIRC published “Supreme Court Judgments on SEBI Act, Rules and Regulations” and “Practical Aspects of Service Tax” in last two months. The other publications on Managerial Remuneration, Non-Banking Financial Companies and Transfer Pricing are proposed to be published in next two months. I compliment CS Prakash Pandya, CS Shailashri Bhaskar and CS Smitesh Desai for their untiring efforts in bringing out the publications.

With the passing of the much awaited Companies Bill by the Rajya Sabha on 8th August 2013, the members have to now gear up to embrace the challenge of re-learning the new Law. The Bill provides for worthwhile recognitions to CS, both in employment and in practice, and at the same time also poses enormous challenges in terms of accountability and responsibilities. All the members are requested to attend the programs on Companies Bill to equip themselves with new provisions without waiting for the Companies Rules to be made public. The Companies Bill now awaits President’s assent. It is hoped that the Companies Rules will soon be made available for consultative process.

I also humbly request all the members to join LIC Group Insurance Scheme of ICSI-WIRC. The details of the Scheme are available with WIRO, Mumbai. The details are also published in this Edition of FOCUS.

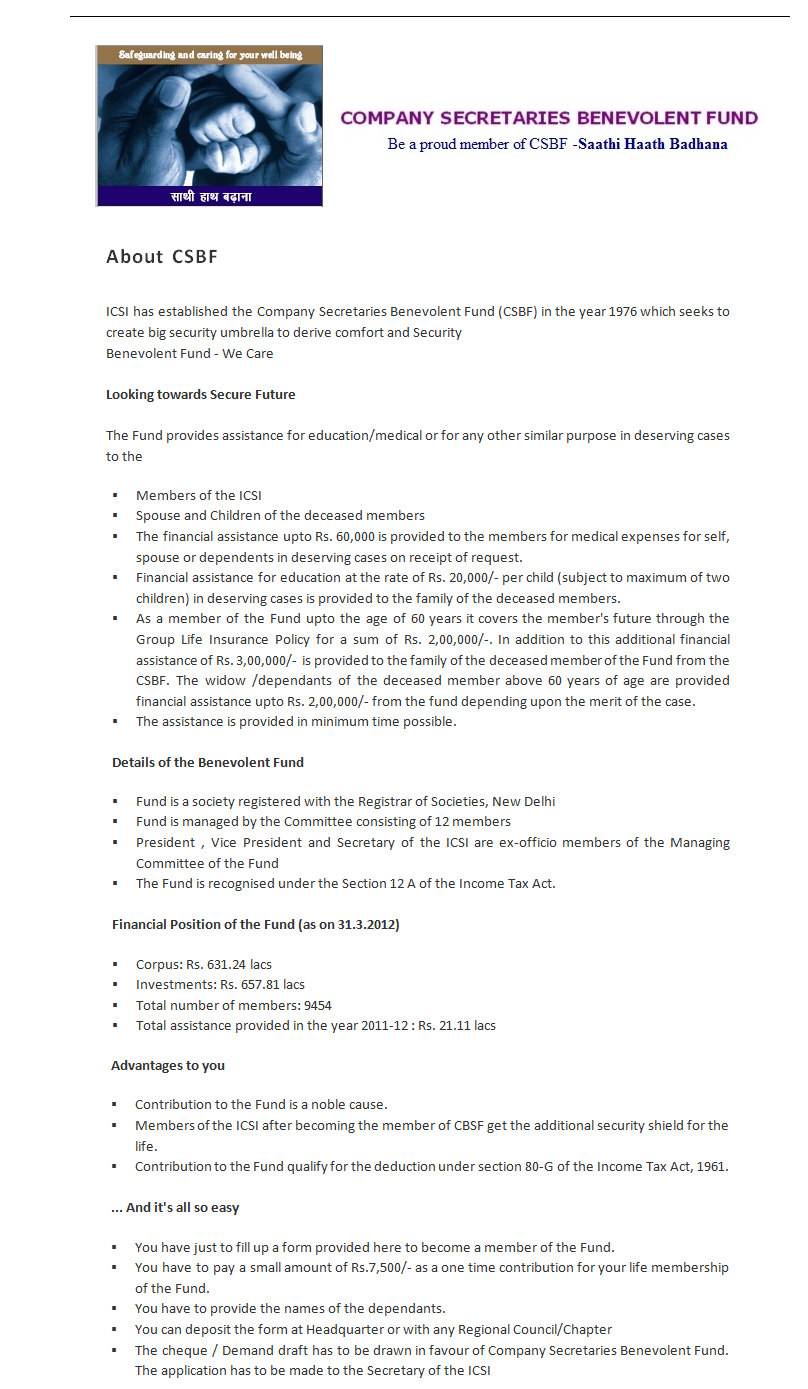

Before concluding, I sincerely appeal the members to join COMPANY SECRETARIES BENEVOLENT FUND, if they have yet not joined.

With Warm Regards,

CS Hitesh Buch

20th August 2013

Editorial Board

Photo Feature

Companies Bill 2012- An introspection

Introduction

The nuances in the Companies Bill 2012 after its passage through the lower house of parliament on December 18,2012 have been debated through the length and breadth of the country in professional forums .After the initial euphoria associated with its passage in the lower House, the bill seems to have gone off the radar, seemingly into an unchartered orbit, as little is now being heard about its movement. The draft Rules were supposed to be released by February 2013 for public debate and last heard, the bill was slated for discussion by the “elders’’ of the House two months ago. All this has triggered off the apprehension that the Bill may crash land, meeting the same fate as its predecessors. We sincerely hope that this does not happen since the Bill,in many ways marks a watershed in that it seeks to replace the existing law which has gone past its ”use by date” tag and was being seen as an anachronism especially against the backdrop of the paradigm shift that India Inc. has been a witness to in recent times. One conspicuous feature that comes out strongly in the Bill is that there is a thematic shift towards making the proposed law “Rule based” a la the laws governing levy of Excise Duty, Service Tax. A substantial portion of the Bill will be through the form of Rules which ought to have been prescribed by now. Administering the substantive law through delegated legislation is a double edged sword. On the one hand, changes can be made to the Rules as considered appropriate without seeking parliamentary sanction. The flip side is the spectre of a trigger happy Bureaucracy which may ring in the changes at the drop of a hat, as it were, thus injecting an element of adhocism to the Legislation which is best avoided. Be that as it may, it can be said at this juncture that no objective evaluation as to the appropriateness of the proposed law is possible unless it is read conjointly with the sub-ordinate legislation to be prescribed through Rules.

The nuances in the Companies Bill 2012 after its passage through the lower house of parliament on December 18,2012 have been debated through the length and breadth of the country in professional forums .After the initial euphoria associated with its passage in the lower House, the bill seems to have gone off the radar, seemingly into an unchartered orbit, as little is now being heard about its movement. The draft Rules were supposed to be released by February 2013 for public debate and last heard, the bill was slated for discussion by the “elders’’ of the House two months ago. All this has triggered off the apprehension that the Bill may crash land, meeting the same fate as its predecessors. We sincerely hope that this does not happen since the Bill,in many ways marks a watershed in that it seeks to replace the existing law which has gone past its ”use by date” tag and was being seen as an anachronism especially against the backdrop of the paradigm shift that India Inc. has been a witness to in recent times. One conspicuous feature that comes out strongly in the Bill is that there is a thematic shift towards making the proposed law “Rule based” a la the laws governing levy of Excise Duty, Service Tax. A substantial portion of the Bill will be through the form of Rules which ought to have been prescribed by now. Administering the substantive law through delegated legislation is a double edged sword. On the one hand, changes can be made to the Rules as considered appropriate without seeking parliamentary sanction. The flip side is the spectre of a trigger happy Bureaucracy which may ring in the changes at the drop of a hat, as it were, thus injecting an element of adhocism to the Legislation which is best avoided. Be that as it may, it can be said at this juncture that no objective evaluation as to the appropriateness of the proposed law is possible unless it is read conjointly with the sub-ordinate legislation to be prescribed through Rules.

In many ways the bill provides a breath of fresh air. For one it has many a novel feature such as the concept of a “one Person company”, it lists out the duties of directors, recognizes the importance of having independent Directors both in listed as also unlisted companies answering to a prescription to be laid down later. By the same breath it has several proposals which strike a discordant note suggesting a need for either revisiting them or to temper them through appropriate subordinate legislation before it receives the presidential nod. In this discussion we shall therefore focus on some of the proposals which do not appear to be in harmony with the objectives of the Bill and perhaps call for a review.

• Clause 2(41)-Financial Year

This clause provides that the financial year for a Company shall be the period ending March 31 each year. Where the company has been incorporated on or after January 1, of a year, the financial year will end on March 31 of the following year, in respect of which the financial statement of the company shall be made up. The above provision is in line with Section 3 in the Income Tax Act, 1961 which provides for a uniform previous year.

Where a Company is the subsidiary or Holding company of a Company incorporated outside India, and is required to follow a different financial year for consolidation of Accounts outside India, upon an application being made by the Company with the Tribunal, if the Tribunal is satisfied , the company may be allowed to follow any period as its financial year. In order to enable a company to fall in line with the above requirement, a transitional period of two years shall be allowed.

The above proposal will take away the flexibility companies hitherto had in the matter of choice of the financial period, albeit only for the purposes of the proposed Enactment. The ushering of a uniform financial year under the Income Tax law in the year 2000 was intended to facilitate, inter alia, fiscal consolidation. One fails to comprehend the need for bringing about uniformity in the financial year in a procedural statute such as the Companies Act. Companies engaged in seasonal industries such as sugar, Tea, normally would normally fix their financial years to end either in June or they would follow the calendar year to even out seasonal fluctuations in their activities.

• Clause 2(87)-Subsidiary Company

This Clause, inter alia ,contemplates that exercise or control over one half of the total Share Capital by one Company either on its own or with one or more of its subsidiaries would make the other Company a Subsidiary. The Clause does not draw any distinction between the class of shares held for the purpose of determining the Subsidiary relationship. Therefore it follows from the above, that preference shares held by a Company in another Company will come into reckoning in determining whether the latter is a subsidiary or not. The above proposal is somewhat intriguing when one considers that Preference Share Capital represents “mezzanine capital” and the holders thereof are not bestowed with voting powers except for those matters which impact their own rights. They are clothed with all the rights of equity holders only when the circumstances envisaged in Clause 47(1) of the bill which corresponds to Section 87(2) in the present Act are visited.

The basic ingredient in a Holding-Subsidiary Company relationship is the capacity of the Holding company to control the other Company generally through the holding of 51% or more of the equity Capital of the latter. Under the proposed law, it may well be that, in a given situation, one Company may hold the entire preference capital of another Company without any Equity holding leading to a situation whereby more than one half of the total share capital of the other Company is controlled by the former. In such a scenario, the latter Company would become a Subsidiary. Assuming that Dividend in respect of the preference shares are not in arrears it may well be that the Holding Company cannot wield control over the other Company simply because it does not have any voting rights!.This would be a paradox and would simply cut across the grain of a Holding company-Subsidiary relationship.

Considering the above, it is earnestly submitted that the status quo ante on the subject is restored and only voting shares namely ,Equity shares be taken into consideration for the purposes of clause 2(87) above.

• Clause 8-Formation of Companies with Charitable objectives

The above clause facilitates the setting up of Companies for “nonprofit “purposes. The basic ingredients in the said clause are substantially identical to Section 25 of the present Act save and except for clause 8(11)which speaks about the levy of penalties for contravention of the provision. The said Clause envisages the imposition of a fine which shall not be less than Rs 10 lacs but which may extend to Rs 1 Crore . In addition, the errant Directors and officers shall be liable to imprisonment for a term which may extend to three years or a fine which may be as much as Rs 25 lacs or to both. We have looked at other punitive provisions of the Bill and it is found that under no other provision is the quantum of penalty as much as in clause 8(11).Unless the intention of the powers that be, is to clamp down completely on the formation of non-profit entities , it is submitted that the above punitive provision be moderated as it is exemplary in nature.

• Mode of redemption of Preference shares-Clause 55(2)(d)

Clause 55(2) in the bill envisages that the Securities premium Account could be used, inter alia, to provide the premium payable on the redemption of Redeemable preference shares. This is consistent with the existing provisions in Section 78 of the present Act. The above facility of using the Securities premium Account for redemption purposes is sought to be taken away by clause 55(d) (i) which proposes that in the case of such class of companies , as may be prescribed and whose financial statements comply with the Accounting Standards as applicable to it in clause 133,the premium on redemption shall be provided out of the profits of the company. It is not clear as to what is the trigger point for denying the benefit of using the Securities premium Account and we shall have to wait for the Rules to be prescribed to appreciate the justification for the above proposal. The immediate fall out of the above proposal would be that the distributable profits of companies which would be covered under the Rules would be impacted if redemption premium has to be met out of their profits.

• Registration of charges-Clause 77

This clause envisages that charges created either in India or outside India by a Company on its properties or Assets both tangible and intangible shall be liable to registration with the ROC. We are aware that u/s 125(4) of the present Act , only certain types of charge are liable for registration with the ROC. It is observed that the bill does not contain a list similar to the one contained in the present Act with the result that all kinds of encumbrances created by a company on its assets shall come within the ambit of registration.

• Postal ballot-Clause 110

A plain reading of this Clause suggests that the requirement of a postal ballot will not only apply to listed companies but also to unlisted companies as well. Further any business other than ordinary business in respect of which the Directors or the Auditor have a right to be heard shall be transacted by a postal ballot. The Central Government shall by notification be empowered to declare the items to be transacted by postal ballot.

As the cost associated with a postal ballot is substantial especially where there is a large investor base, ,it is hoped that the Central Govt will while issuing the required notification, consider the ground realities and make the above requirement applicable only to companies of a reasonable size and prescribe appropriate thresholds.

• Consolidation of Accounts-Clause 129(3)

The above clause provides that where a company has one or more subsidiaries, it shall , in addition to its stand alone financial results, prepare consolidated financial statements of itself along with its subsidiaries and these statements will have to be placed at the Annual General Meeting of the Company. Explanation to the above clause clarifies that for the purposes of this clause, the term ”Subsidiary “shall include an Associate company and Joint ventures. The Central Government has been empowered in terms of the above clause to prescribe the manner of consolidation .

It follows from the above that presentation of consolidated Accounts will not be a requirement which will be restricted to listed companies alone. As consolidation of Accounts entail additional costs, it will turn out to be an expensive proposition. It is therefore expected that while laying down the modalities for consolidation, the Central govt. shall ensure that no undue hardship is created to marginal and small sized companies which have Subsidiaries.

• Board’s Report-clause 134(1)

A slew of new items are proposed to be added to the Board’s Report some of which overlap with the requirements of clause 49 where it come to listed companies. In order to avoid tedium and redundancy in compliance, it is imperative that the provisions of clause 49 are aligned with the bill. For the sake of brevity we are not reproducing in this exposition the additional items which need to be included in the Board’s Report.

• Appointment of Auditors-clause 139(1)

The above clause envisages that the statutory Auditors shall be appointed at the first Annual General Meeting (AGM) to hold office from the conclusion of that meeting till the conclusion of its sixth AGM. In effect the appointment shall be for a period of five years. Proviso to the said Clause states , however, that the Company shall place the matter relating to such appointment for ratification of members at every AGM. It is not clear from the proviso whether the ratification of the members is to be secured by an appropriate resolution or merely by way of a noting in the minutes of the Meeting. Logically it should be through a resolution. If this is so, we see a dichotomy in the proposals based on a conjoint reading of the above Clause with Clause 102 (2) which sets out the items of ordinary business to be transacted at the AGM. Sub-clause (iv) to Clause 102(2) provides that the appointment of and the fixing of the remuneration of the auditors would be an item of ordinary business. As the Auditors’ term is to be for a period of five years, obviously it would not be necessary to propose their re-appointment at each AGM during the above tenure of five years. What would be necessary , however, would be to seek the ratification of members at each AGM of the appointment as envisaged by the proviso to clause 139(1) as referred to above. Seeking ratification of the members to the appointment of the Auditor does not figure in the list of items to be transacted as “ordinary business”. Ratification of members cannot obviously be part of “special business”.

In view of the above, perhaps it would have been better if Sub-clause(iv)to Clause 102(2) were reframed to read as under:

“the appointment and /or ratification of the appointment of …………..the Auditors”. Alternatively , the law will have to be “read down” in a manner that the term ”appointment” shall include ratification as well.

• Corporate Social Responsibility-Clause 135(1)

In our view, the proposal that every Company satisfying the prescribed criteria should ensure that there should be CSR spends for at least 2% of the average net profits of the Company during the last three years calls for a review as it will impact the distributable profits of companies. 2% of Net Profits for large Corporations represents a substantial amount. It would have been better to prescribe an appropriate threshold for CSR spends for a period of say five years as opposed to insisting on yearly spends. It is also necessary to ensure that Companies get tax breaks against the CSR spends through the introduction of appropriate provisions in the Income Tax Act, 1961.

• Remuneration of Auditors-Clause 142(1)

The remuneration of the Auditors shall be fixed at the Company’s General Meeting or in such manner as may be determined therein. The proviso to the above Clause stipulates that the Board may fix the remuneration of the first auditor appointed by it. A plain reading of the above suggests that the Board shall be authorized to fix the remuneration of the First auditors only as they are appointed by it. Given the fact that the Bill provides for the appointment of the Auditors for a five year period, it would not be proper if the Shareholders were made to decide on the remuneration of the Auditors for a five year horizon at the time when they approve of their appointment . It is necessary that the decision as regards the remuneration payable to the Auditor should be delegated to the Board and the Rules to be laid down on this should facilitate the continuance of such procedure.

• Resignation of Director-Clause 168

Proviso to the above clause stipulates that the Director demitting his office , should forward a copy of his resignation along with the detailed reasons for his resignation to the ROC within 30 days of his resignation.

In our view the onus of informing the ROC about the resignation should continue to be that of the Company and the requirement of the Director sending a copy of his resignation to the ROC should be dispensed with.

The fact that sub-clause (2) to clause 168 clarifies that the resignation shall take effect from the date on which notice is received by the Company or on the date specified by the director in the notice whichever is later suggests that the resignation of the Director would take effect regardless of whether he has sent to the ROC a copy of his resignation.

• Loans and Investment by Company- Clause 186

The above Clause corresponds to Section 372A in the present Act. The bill proposes to make the provision applicable to private companies as well. Further loans, investments, guarantees extended by a Holding Company in favour of its wholly owned subsidiaries will not be exempt from the purview of the above clause. This proposal may cause hardships to Companies big and small alike.

• Related Party Transactions-Clause 188

Related party transactions including those involving lease/transfer of property of any kind will be subject to approval by the Board , subject to such conditions as may be prescribed. In order that fetter proposed to be imposed through this clause may be meaningful it is necessary that the sub-ordinate legislation to be prescribed should be such as to provide for realistic thresholds in terms of value so that every transaction with a related party is not subjected to the rigmarole of a Board sanction.

• Class Action-Clause 245

An application for class action against the company can be preferred with the Tribunal by members or deposit holders in case the Company is being managed or the conduct of its affairs are being conducted in a manner which is prejudicial to the interests of the company ,its members or its depositors. Such action can be resorted to by not less than 100 members or not less than such percentage of members as may be prescribed or by members holding such percentage of the issued capital as may be prescribed. A similar criteria would apply where such action is preferred by Depositors. Lest the provision should be perpetrated to abuse by stakeholders who may have an axe to grind, it is imperative that realistic thresholds are prescribed for determining the eligibility to class action so that the remedy is resorted only in compelling circumstances.

Conclusion

We have cherry picked on some of the provisions in the bill to drive home the need for a possible review primarily with a view to eliminate the possibility of any hardship being caused to the companies and the stakeholders alike. The bill does contain quite a few laudable features which will go towards enhancing the levels of governance and transparency. We can debate as they say, until the cows come home on the appropriateness of the changes proposed in the new legislation. Law can never be a panacea for social ills, much less a procedural law which seeks to regulate the functioning of corporations. We will therefore leave it for posterity to pass judgement on the suitability or otherwise of the proposed law which seeks to replace an antiquated piece of legislation which has stood the test of time.

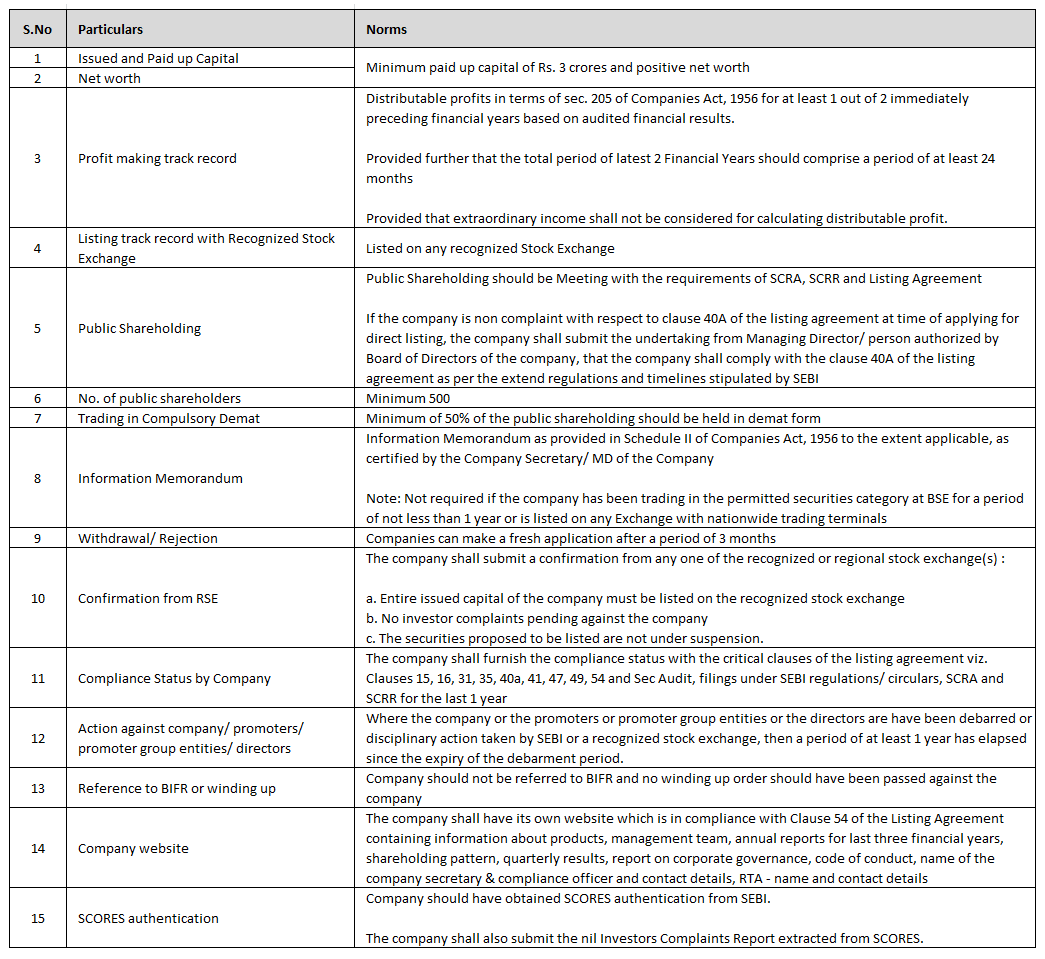

BSE Direct Listing – Value Unlocking Opportunity

The Indian Government has to be credited for regularly taking different measures since its independence to ensure overall development of capital markets in India. One such distinct initiative was introduction of regional stock exchanges across different states in order to increase confidence level of local investors who were scared of investing in IPOs of new companies. It was also made mandatory for every company to get listed on their respective regional stock exchange while coming out with an IPO. Needless to mention, many regional stock exchanges were set up for a variety of tax and other reasons. At one point of time, India used to boast of having nearly 2 dozen active stock exchanges spread across different states of the country.

The Indian Government has to be credited for regularly taking different measures since its independence to ensure overall development of capital markets in India. One such distinct initiative was introduction of regional stock exchanges across different states in order to increase confidence level of local investors who were scared of investing in IPOs of new companies. It was also made mandatory for every company to get listed on their respective regional stock exchange while coming out with an IPO. Needless to mention, many regional stock exchanges were set up for a variety of tax and other reasons. At one point of time, India used to boast of having nearly 2 dozen active stock exchanges spread across different states of the country.

However, with the aggressive expansion by 2 national level exchanges i.e. Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) by increasing their membership base and opening their trading terminals across the country over last few years, these regional stock exchanges have gradually lost their relevance. Moreover, it is no longer compulsory for the companies to get listed on a regional stock exchange which makes the situation even more vulnerable for the regional stock exchanges. In fact, most of the regional stock exchanges have ‘nil’ trading for last several years and there is a remote possibility of having trading in the nearby future. Shareholders of the companies listed exclusively on regional stock exchanges currently do not have any exit option and hence, there is limited possibility of value unlocking for them.

SEBI issued a circular in May 2012 to make it very clear that risk mitigation is very important for all the stock exchanges and simultaneously introduced strict norms for own clearing corporation, minimum paid-up capital, shareholding pattern, restriction on brokers on holding stake, etc. SEBI has taken a firm stand and advised all the stock exchanges to comply with the basic eligibility norms if they wish to continue their operations. Alternatively, an option was provided to them for voluntary wind-up.

In the event of winding-up of a regional stock exchange, it would be a great loss to the companies listed on them as well as their shareholders. Hence, in consultation with SEBI, the BSE has introduced new ‘Direct Listing’ mechanism for the companies listed exclusively on regional stock exchanges by prescribing basic eligibility norms. Every company which fulfils following norms can submit a formal application to BSE for getting listed on its main board alongwith necessary supporting documents:

It is estimated that there are around 10000 listed companies in India, however, merely half of them are listed on BSE. ‘Direct Listing’ provides an unique opportunity for remaining 5000 companies listed on regional stock exchanges to migrate to BSE and create value for all the stakeholders.

Since ‘Direct Listing’ is a new initiative, the process is yet to get stable. If all the documents are available and necessary compliances are being done by the company, the process can be completed in a span of 3 to 6 months. Due to limited awareness, not many companies have come forward so far for getting listed on BSE. However, it would be recommended for companies listed on regional stock exchanges to take quick action for tapping this golden opportunity and get first-mover advantage before there is change in the eligibility criteria by the market regulators.

Understanding: “Disposal” & “Undertaking” – In terms of Section 293 (1) (A) of the Companies Act, 1956.

(Part - II)

In the Part I, we discussed in detail the provisions of Section 293 (1) (a) of the Companies Act, 1956 (“the Act”); the objectives of the Section and the expression “otherwise dispose of”.

In the Part I, we discussed in detail the provisions of Section 293 (1) (a) of the Companies Act, 1956 (“the Act”); the objectives of the Section and the expression “otherwise dispose of”.

In this part, we will discuss the expression “Undertaking”, the Accounting Treatment of transactions falling under the provisions of Section 293 (1) (a) of the Act and the applicability of the Section.

“UNDERTAKING”

Another important expression in Section 293 (1) (a) of the Act is “Undertaking”. Whether “undertaking” means selling its assets, settling liabilities, termination of operation by abandonment, closing of facilities, abandoning product or product lines, change in size of work force at a particular location?

In order to deliberate more on the expression, let us review few of the landmark judgements:

1) P S Offshore Inter Land Services Private Limited V/s Bombay Suppliers & Services Limited :

The Company was engaged in the activity of oil exploration and offshore drilling of oil. It owned three vessels for the purpose of its business. One of the vessels was remaining idle and creating problems of operational expenditure, therefore the Board of Directors of the company decided to sell that vessel. Was it necessary to obtain the consent of the shareholders of the company under Section 293 (1) (a) of the Act?

The Bombay High Court held that “the expression ‘undertaking’ used in this Section is liable to be interpreted to mean ‘Unit’, the business as a going concern, the activity of the company duly integrated with all its components in the form of assets and not merely some asset of the undertaking. Having regard to the object of the provision, it can, at the most, embrace within it all the assets of the business as a unit or practically all such constituents. If the question arises as to whether the major capital assets of the company constitute the undertaking of the company while examining the authority of the Board to dispose of the same without the authority of the general body, the test to be applied would be to see whether the business of the company could be carried on effectively even after disposal of the assets in question or whether the mere husk of the undertaking would remain after disposal of the Assets?

It is, therefore, possible to take a view that the board of directors cannot dispose of ‘all the capital assets of the company’ taken together which will denude (meaning – discard /uncover) the company of its business or will leave merely the husk behind.

Thus, it is not possible to treat merely one of the assets of the company as an ‘Undertaking’ within the meaning of Section 293(1) (a) of the Companies Act, 1956”. This is a landmark judgement which provides adequate clarity on the expression “undertaking”.

2) Yallamma Cotton, Woollen & Silk Mills Co Ltd :

In this case, the Mysore High Court held that the word ‘undertaking’ is not in its real meaning anything which may be described as a tangible piece of property like land, machinery or the equipment; it is in actual effect an activity of man which is commercial or business parlance means an activity engaged in with a view to earn profit. The property, whether movable or immovable, used in the course of or for the purpose of business can more accurately be described as the tools of business or undertaking, i.e., things or articles which are necessarily to be used to keep the undertaking going or to assist the carrying on of the activities leading to the earning of profits.

3) International Cotton Corporation (Private) Limited Vs Bank of Maharashtra :

In this case, the Mysore High Court upheld the decision in “Yallamma Cotton, Woollen & Silk Mills Co Ltd.” and held that the word “Undertaking” has been defined as “any business or any work or project which one engages in or attempts as an enterprise analogous to business or trade”. The business or undertaking of the company must be distinguished from the properties belonging to the company. In this case, it was only the properties belonging to the company that had been dealt with by the Board of Directors under the deeds of hypothecation and mortgage in favour of the bank. The learned judge held that no part of the undertaking of the company was disposed of in favour of the Bank.

4) Brooke Bond India Ltd. v. U.B. Ltd :

In this case the Bombay High Court held that the sale of shares (in whatever quantity); even if it amounts to a transfer of the controlling interest of a company, cannot be equated to the sale of any part of the "Undertaking" in terms of Section 293 (1) (a) of the Act.

In this case, there was an agreement between the two companies for sale of a specified number of shares of another company. Even though in the agreement; there was use of expression like “sale of food business” of the seller to the purchaser; the Judge held that the agreement contemplated the sale of controlling shares in the company and accordingly held that the sale of shares, whatever be their number (even it is the controlling interest in a company); cannot be equated to the sale of any part of the "undertaking" so as to come within the purview of Section 293(1)(a) of the Act.

APPLICABILITY:

The provisions of Section 293 of the Act are applicable to:

1) Public Company and;

2) Private Company which is a subsidiary of Public Company.

The provisions of Section 293 of the Act are not applicable to Private Company. However, if the Articles of Association of the Private Company contains such restrictions (as prescribed under Section 293 of the Act) on the powers of the Board of Directors of the Company then the consent of the members shall be obtained by such Private Company.

OTHER RELATED PROVISIONS OF THE COMPANIES ACT, 1956:

Pursuant to the provisions of Section 293 (2) of the Act, the provisions of Section 293 (1) of the Act shall not affect in following cases:

(a) Where the buyer / person one who takes on lease such undertaking in good faith; or

(b) Where the ordinary business of the company consists of selling or leasing of properties.

Pursuant to the provisions of Section 293 (3) of the Act, the resolution passed under Section 293 (1) (a) of the Act may contain certain conditions that need to be fulfilled. Such conditions may relate to the use, disposal and investment of the sale proceeds which may result from the transaction.

A listed company may ensure compliance of the provisions of Section 293 (1) (a) of the Act by passing a resolution by Postal Ballot in accordance with the provisions of Section 192A of the Act and Companies (Passing of the Resolution by Postal Ballot) Rules, 2001.

RELATED PROVISIONS IN THE COMPANIES BILL, 2012:

The Clause 180 of the Companies Bill, 2012 (As passed in the Lok Sabha) relates to “Restrictions on powers of the Board”. In the Explanation to Clause 180 (1) (a) of the Companies Bill, 2012; two important expressions have been explained as follows:

(i) “Undertaking” means an Undertaking in which the investment of the company exceeds 20% of its Net Worth as per the audited balance sheet of the preceding financial year OR an Undertaking which generates 20% of the Total Income of the company during the previous financial year;

(ii) “Substantially the Whole of the Undertaking” in any financial year shall mean 20% or more of the value of the Undertaking as per the audited balance sheet of the preceding financial year.

ACCOUNTING ASPECT:

The Accounting Standard (AS) 24 issued by the Institute of Chartered Accountants of India (ICAI) relate to “Discontinuing Operations”. The Objective of AS 24 is to establish principles for reporting information about discontinuing operations, thereby enhancing the ability of users of financial statements to make projections of an enterprise's cash flows, earnings-generating capacity, and financial position by segregating information about discontinuing operations from information about continuing operations.

Clause 3 of AS – 24 defines “Discontinuing Operation”. It is a component of an enterprise:

1) Which pursuant to a single plan, proposes to:

i) Dispose of the component substantially by selling the component in a single transaction or by Demerger or Spin - Off of ownership of the component to the enterprise's shareholders; or;

ii) Dispose of in a piecemeal manner the component's assets and settling its liabilities individually;

iii) Termination by abandonment.

2) Which represents a separate major line of business or geographical area of operations;

3) Which can be distinguished operationally and for financial reporting purposes.

In my view, the scope of AS 24 is wider the scope of Section 293 (1) (a) of the Act because it includes disposing of a component by way of demerger or spin off and disposal by way of abandonment.

With respect to the discontinuing operations of a company; the AS 24 also explains about the recognition and measurement, disclosures (initial / others / updating the disclosure/ separate disclosure for each discontinuing operation) in the financial statement of the company.

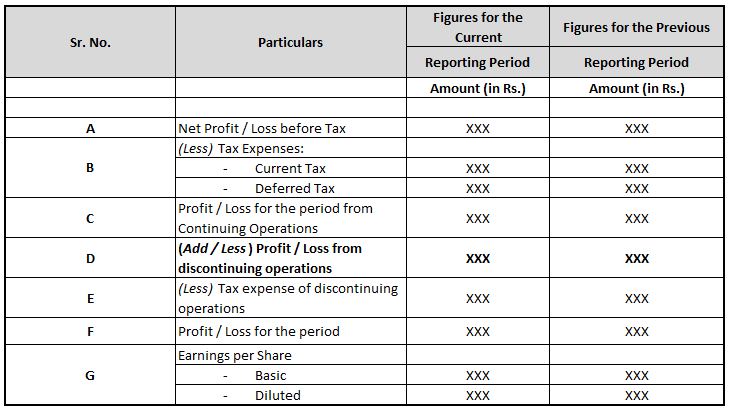

DISCLOSURES AS PER REVISED SCHEDULE VI:

In accordance with the revised Schedule VI of the Companies Act, 1956; the disclosure of the discontinuing operations are made as follows:

CONCLUSION:

The expression of “Undertaking”, as discussed above, shall not be applied as a thumb rule. The above cases can definitely be referred to as guiding principles but it shall be concluded as an “Undertaking” only after considering the facts of the case.

It is very necessary to know and understand the provisions of Section 293 (1) (a) of the Act as it is one of the ways of corporate restructuring. Also, knowing the accounting as well as the income tax aspect is important to assist the management of a company in taking informed decisions.

Role of Company Secretary under new Companies Bill 2012

It’s a matter of great pleasure for all professionals that we are about to enter in a new era of new companies act. This era is about to bring so many new opportunities for CS profession. The new Companies Act emphasizes more and more to non quantitative data in financial statements. Here are some of the important provisions which are likely to raise the opportunities of CS profession:

It’s a matter of great pleasure for all professionals that we are about to enter in a new era of new companies act. This era is about to bring so many new opportunities for CS profession. The new Companies Act emphasizes more and more to non quantitative data in financial statements. Here are some of the important provisions which are likely to raise the opportunities of CS profession:

1) For the first time in the Companies Act, the clear cut definition of “Expert” has been given and Company Secretary has been included under the term “Expert”.

2) Applicability of Secretarial Standards to all companies with regards to Board meetings and General Meetings.

3) Every company shall prepare a return (hereinafter referred to as the annual return) in the prescribed form containing the particulars as they stood on the close of the financial year regarding its registered office, principal business activities, holding of Subsidiary and associate companies, share, debentures and other Securities, indebtness, its members and denture holders, its promoters, directors, key managerial personnel along with changes therein since the close of the previous financial year; meetings of members or a class thereof, Board and its various committees along with attendance details; remuneration of directors and key managerial personnel, penalty or punishment imposed on the company, its directors or officers and details of compounding of offences and appeals made against such penalty or punishment, matters relating to certification of compliances, disclosures as may be prescribed, details, as may be prescribed, in respect of shares held by or on behalf of the Foreign Institutional Investors indicating their names, addresses, countries of incorporation, registration and percentage of shareholding held by them; and such other matters as may be prescribed and signed by a director and the company secretary, or where there is no company secretary by a company secretary in practice:

Provided that in relation to One Person Company and small company, the annual return shall be signed by the company secretary, or where there is no company secretary, by the director of the company.

Till now it is mandatory only for listed companies to get signed their annual return from Company Secretary. But after the commencement of New Companies Act, it will mandatory for all companies to get signed their annual return either from Whole-time Company Secretary in employment or from a Company secretary in practice. Even one person Company and small companies are also given the provision to sign their annual return from Company Secretary. On the other hand giving details of non-financial data like giving details of its members and debenture holders and giving details of meetings of members or a class thereof, Board and its various committees along with attendance details would obviously require the professional capacity of Company Secretary.

Purchase of immovable property in India by a person resident outside India

Now a days, we can observe that there is lots of boom Real Estate Sector of the Indian Market and due to which many of the NRI’s, PIO’s and Foreign Nationals are investing in India for purchasing of immovable property in India especially in the regions of Goa.

Now a days, we can observe that there is lots of boom Real Estate Sector of the Indian Market and due to which many of the NRI’s, PIO’s and Foreign Nationals are investing in India for purchasing of immovable property in India especially in the regions of Goa.

However, they are having lots of confusion related to RBI guidelines related to purchase of property in India. In order to simplify the RBI procedures, RBI has issued a master Circular No. 04/2013-14 Dated 01st July, 2013 related to Acquisition and Transfer of Immovable Property in India by NRIs/PIOs/Foreign Nationals of Non-Indian Origin and the regulations made thereon.

To simply the understanding of the above said issues please have a look on the following article.

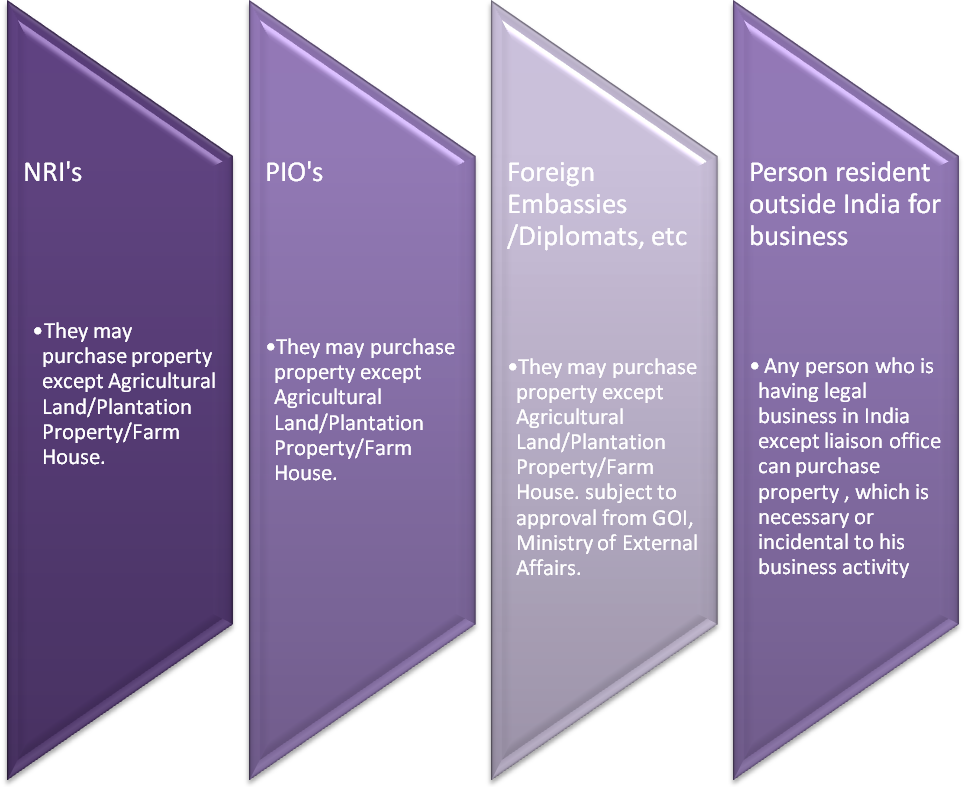

1. Person entitled to purchase immovable property in India.

2. Consideration for purchase immovable property in India.

As we have seen who are entitled to purchase immovable property in India. But for purchasing they have to pay certain consideration to purchase these assets. Since, they are NRI’s/PIO’s or any foreign national they have to bring money by proper banking channel as fixed by the RBI for each and every category.

1) NRI’s and PIO’s.

i)Purchase out of funds received by inward remittance through normal banking channels or by debit to his NRE / FCNR(B) / NRO account.

ii)However it may be noted that payments cannot be made either by traveller’s cheque or by foreign currency notes or by other mode other than those specifically mentioned above.

2) Foreign Embassies/Diplomats/Consulate Generals.

i)Consideration for purchase of immovable property in India is paid out of funds remitted from abroad through the normal banking channels.

3. Reporting Requirement for purchase to RBI.

If the purchaser is NRI or PIO then general permission is being granted by RBI for purchase of immovable property and no reporting is required by them.

However, if person resident outside India for carrying on a permitted activity have to file a declaration in form IPI to the Authorised Dealer within 90 days from the date of purchase alongwith the following documents:-

i)Copy of Registration documents of the property;

ii)Evidence and source of payment given to seller;

iii)If the buyer is a corporate then in that case copy of Board Resolution for authorising a person to purchase property mentioning purpose to purchase;

iv)Particulars of seller;

v)Any other documents which differs on case.

Further, citizen of Pakistan, Bangladesh, Sri Lanka, Afghanistan, China, Iran, Nepal or Bhutan, whether resident in India or outside India cannot acquire property in India without prior approval of RBI. However, if these people take the property on lease for not exceeding 5 years then this restriction is not applicable.

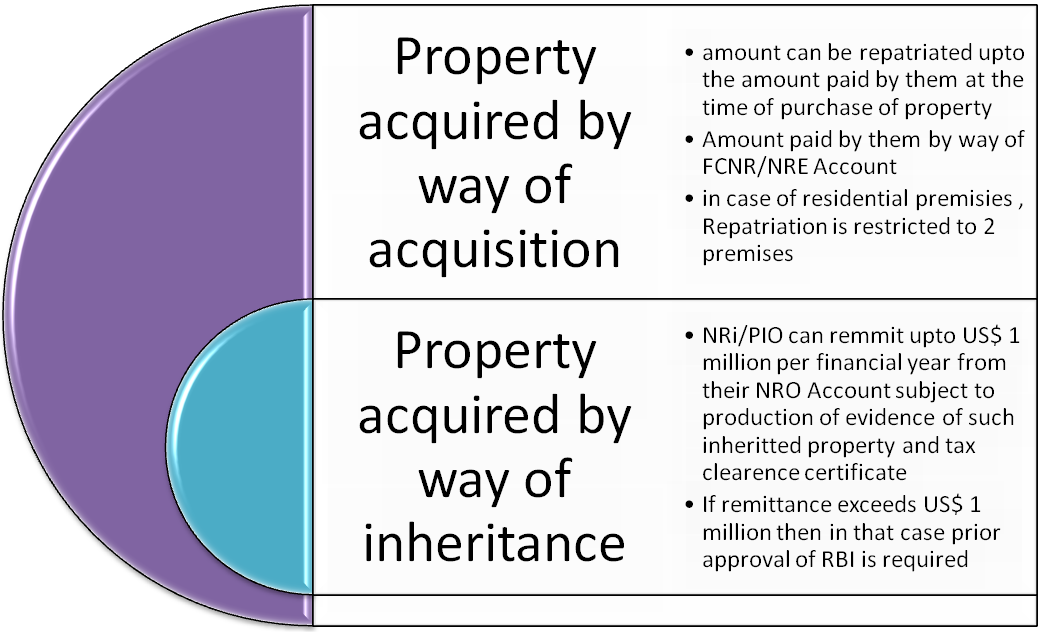

4. Repatriation of sale proceeds of the property.

Any person who is holding immovable property and is not residing in India, then in that case they may remit funds back to the abroad with certain terms and conditions as laid by the RBI which can be understood with the help of example:-

Mr. A presently resides in United States and owner of one residential premise in Indore which he has purchased 10 years when he resides in India Only. Further after the demise of his father another residential premise was received by him inheritance.

Now he wants to sell both of these premises and want to repatriate this fund from India to US.

Answer to his problem can understood with the help of this diagram

How to combat Cold & Flu

Monsoon brings wonderful respite from months of heat and most of us revel in everything that comes with the season….rained washed surroundings, piping hot pakodas with hot chai, and sharing a roasted bhutta with loved ones. But, the season also brings with it a host of illnesses that afflict a majority of us unless we are very cautious.

Monsoon brings wonderful respite from months of heat and most of us revel in everything that comes with the season….rained washed surroundings, piping hot pakodas with hot chai, and sharing a roasted bhutta with loved ones. But, the season also brings with it a host of illnesses that afflict a majority of us unless we are very cautious.

Cold and flu are among the most common problems in this weather, and often we find it difficult to distinguish between the two.

What is the difference between a cold and the flu?

Although the flu and the common cold are both respiratory illnesses, they are caused by different viruses. Because they have similar symptoms, it can be difficult to tell them apart. But generally cold symptoms are much milder than flu.

Common cold symptoms include:

• Sore throat

• Stuffy nose

• Runny nose

• Cough

• Mild fever

The flu, on the other hand, often causes higher fever, chills, body ache, and fatigue.

Nutritionist Mruga Dholakia presents some tips to prevent colds and flu, and natural remedies to tackle the conditions!

1. Cold and flu usually spread through direct contact; for example, if a person sneezes on his/her hand, and later touches other surfaces like a keyboard, kitchen implements, etc. The germs can live for hours -- in some cases weeks -- only to be picked up by the next person who touches the same object. So, wash your hands often with soap or liquid wash. If water is not available, carry soap napkins or a sanitizer.

2. Don't cover your sneezes and coughs with your hands to prevent passing on the germs. Try to use a handkerchief, napkin or paper towel instead.

3. Drink plenty of fluids (water, vegetable soups and fruit juices) to replenish the fluids lost during the illness. It is also important to consume plenty of fresh fruits and vegetables as they abound in nutrients which strengthen the immune system. Try not to cook the vegetables for a longer period as this will result in loss of volatile nutrients like vitamins B and C.

4. Avoid smoking as it aggravates the throat and interferes with the infection-fighting activity of cells.

5. It is important to relax and allow body to fight against the virus. For that, you may need to stay away from the dusty environment.

Natural Remedies

Here are some soothing natural remedies that will help keep the doctor away.

a) Turmeric Powder: Medicinal properties of turmeric are because of the presence of compound called Curcumin. It is anti-inflammatory, anti-viral and anti-fungal and thus helps to prevent cold and cough. Have 1 glass of Haldiwala Doodh everyday to get rid of cold/cough.

b) Vitamin C rich fruits: People have a myth to avoid vitamin C rich fruits during cold and cough. But let me tell you that fruits like amla, oranges, strawberries, lemon etc helps to fight virus and decreases the duration of the illness by increasing the body’s immunity levels.

c) Ginger (adrak): Adrakwali chai...this is our favourite drink during monsoons. It soothes our throat and brings warmth to the body. Ginger tea is also an effective remedy against cold.

d) Garlic (lehsun): Garlic is a real immunity booster. Finely chop 2 to 3 cloves of garlic and swallow it like any other medicine. It can also be used raw in salad dressings. Crushing a clove of garlic into soups, stews, etc. is also effective and greatly enhances their flavour.

f) Tulsi (Indian basil): Ancient people used to consume Tulsi as a mouth freshener...no wonder they always hardly faced problems related to cold and cough. A teaspoon of tulsi juice combined with one teaspoon of ginger juice and ¼ teaspoon of honey helps to ease cough.

And yes, Stay close to your Family and Friends...I am sure they will make you feel Special!!

Tax Shield on CSR spendings

The long awaited Companies Bill seeking to transform and accentuate growth of Corporate Sector in India has finally been passed in both Houses of Parliament while waiting for the Hon’ble President’s accent, before it becomes an enactment. One of the most candid provisions enshrined in the Bill relates to Corporate Social Responsibility of Boards of India INC. Every Company whether Private or Public, Listed or Unlisted having a Net worth of Rs.500 Crores or more or turnover of Rs.1000 Crores or more or a Net Profit of Rs.5 Crores or more have to spend on CSR activities prescribed under Schedule VII of the Companies Bill, at least 2% of the average net profits of preceding three years. The company through a special CSR committee constituted will have to explain to the shareholders in its Annual Report if the spending are not made in accordance with the law and the rules made there under.

The long awaited Companies Bill seeking to transform and accentuate growth of Corporate Sector in India has finally been passed in both Houses of Parliament while waiting for the Hon’ble President’s accent, before it becomes an enactment. One of the most candid provisions enshrined in the Bill relates to Corporate Social Responsibility of Boards of India INC. Every Company whether Private or Public, Listed or Unlisted having a Net worth of Rs.500 Crores or more or turnover of Rs.1000 Crores or more or a Net Profit of Rs.5 Crores or more have to spend on CSR activities prescribed under Schedule VII of the Companies Bill, at least 2% of the average net profits of preceding three years. The company through a special CSR committee constituted will have to explain to the shareholders in its Annual Report if the spending are not made in accordance with the law and the rules made there under.

While this is a commendable feature of the Legislation, it is imminent for the Government to legislate a separate set of provision under the Income Tax Act,1961 to provide for corporate tax shield. It must be explicitly understood that the Corporate would not donate or spend largely on CSR unless tax deductions is available to the entity.

Finance Minister Mr. P. Chidambaram will have to move a step forward and navigate cogently to bring out framework in the Income Tax Act which will have to be knitted or fabricated with the rules and guidelines on CSR to be framed by MCA. Any haste made therein would vitiate the very purpose of CSR spends.

One of the moot question would be to ascertain the permissibility or otherwise of the tax expenditure in the favor of Capital Expenditure, while there would be less ambiguity in relation to the revenue expenditure, most of the CSR spending classified under Schedule VII relates to Capital expenditure. For instance, clause (ii) of schedule VII relates to promotion of education. In the manifestation of such a CSR spending, the company may contemplate building a school/college to impart education to a large number of students and may incur capital expenditure or expenditure of enduring advantage. How do the Company treat such expenditure under the Income Tax Act? Another instance could be of building a Hospital to combat health hazards.

Whether donations made under CSR spending to certain special Charitable Institutions of national importance would qualify for weighted deductions. Whether special purpose vehicles (SPV’s) would be framed for donations to NGO’s/Trusts.

Section 37 of Income Tax Act deal with expenditure made wholly and exclusively for the purpose of the business. How do a Company convince the Tax Authorities that these spends would qualify for deductions as business expenditure. The Ministry of Finance and CBDT should issue clarifications in the absence of which no stimulus of CSR spending would take place.

The Appellate Authority/ Courts have always held on this point under the Income Tax Act that the expenditure made should relate directly to the activities of the business so as to qualify for deductions. In case of CSR spending no relation of that sort could be established or actual CSR spending maybe outside the realm of business. For instance, a Textile Company may spend on building an Institution, for promoting Vocational skills related to Realty industry. The contribution to such CSR spends could be purely out of compulsion and not voluntary. MCA, it is hoped, will soon come out with steer-clear guidelines and rules on CSR spends, which will be generally acceptable to Companies, the Tax Authorities and finally within the framework of Company Law.

There is a probability that out of pure compulsion of CSR spending under the Companies Act provision, a company may land up in following suit of other companies, while there are ample opportunities to spend business related Corporate Social Welfare activities.

Scope Of Section 209 – A : Inspection Of Books Of Account Etc. Of Companies

1) The objective of Sec.209 A is to allow Central Government to ensure proper administration of the Companies Act, 1956 and to ensure that the Companies maintain the prescribed books of Accounts and other Registers as mandated under the law.

1) The objective of Sec.209 A is to allow Central Government to ensure proper administration of the Companies Act, 1956 and to ensure that the Companies maintain the prescribed books of Accounts and other Registers as mandated under the law.

2) Section 209A of the Companies Act, 1956 is one of the important provisions that are intended to prevent and / or unearth fraud. The others are Sec.234 (Power of ROC to call for information / inquiry), Sec 237 (investigation of affairs of the company), Sec.217 (2AA) (a statement of satisfaction by the Board of Director that no fraud has come to their notice and that in their opinion sufficient systems / check and balances are in place to prevent and detect frauds, Audit Reports / CARO, 2003 requiring certification of Auditors that proper books of Accounts as required by law have been kept and a categorical statements as to whether any fraud on or by the company has been noticed or reported during the course of their audit etc.

3) Powers of Inspection by Officers of the Government or the Registrar is not restrictive but covers companies of all categories.

4) SEBI can inspect only on matters relating to Section 55A and inspection by SEBI is therefore restrictive in scope and jurisdiction.

5) The Registrar referred to above should have jurisdiction over the company.

6) The Government Officer so authorized need not necessarily be in the employment of the Ministry of Corporate Affairs.

7) The Section is applicable to both public and private companies as well as Government Companies. Foreign companies referred to in section 591 also fall within the purview of this section by virtue of provisions of section 600(3)(b).

8) It is not necessary for the Registrar or the Central Government to disclose to the company, the reasons for conducting the inspection.

9) The inspection under this section is not as investigation as laid down under sections 235 and 237 of the Act, but could lead to one. But the inspection report could result in the Central Government laying the information to police for the purpose of investigation under Criminal Procedure Code instead of proceeding with investigation under the above sections of the Act. (Indian Express (Madurai) Pvt. Ltd. Vs. Chief Presidency Magistrate (1974) 44 Com. Cases 106.)\

10) The Books of Accounts and other Books and Papers are subject to inspection. According to Sections 2(8) of the Companies Act, Act, 1956, Books and Paper are defined to include Accounts, Deeds, Vouchers, Writings and Documents.

11) The Department has clarified that the inspecting officer has a right to examine the books and records of any firm in which the company is a partner. (Letter NO. 7/9/74-CL-II dated 24.01.1976) and books and records of any joint venture in which the company has some interest. (Circular No. 25/75 dated 19.11.1975)

12) No previous notice is required to be given for carrying out inspection. But the inspection should be done during business hours.

13) Administratively, there are several types of inspections viz. full fledged inspection, supplementary inspections and limited inspections. The Order of the Central Government specifies the scope of inspection of a particular company.

14) Under Sections 209-A (2) every director or other officer or employee of the company has to produce books of accounts and other books and papers of the company in his custody or control. Hence a non-executive director cannot be forced to produce books and papers not in his custody or control.

15) The section does not lay down any time limit within which the inspection has to be completed or report to be submitted. But the same should be completed within a reasonable time.

16) Unlike the requirements of section 241 (concerning investigation); the inspection report is not required to be forwarded to the company by SEBI or the Central Government, as the case may be.

17) The offence under this section is not compoundable under section 621A.

18) The Inspecting Officers can take copies of the Books or place marks of identification thereon. They are endowed with the powers of civil courts such as (1) discovery and production of books of account etc. at such place and at such time as may be specified, (2) summoning and enforcing attendance of persons and examining them on oath and (3) Inspecting any books, registers, or other documents of the company at any place.

19) The Inspecting Report is not a public document. Hence, the Central Government can claim ‘privilege’ and refuse to part with the same except under orders of the Court. CIC held under RTI Act that inspection report is a confidential document and hence is not a information available under public domain.

20) Penalties for non-compliance --- 1) Any person who gives a false statements to the Inspecting Officer shall be liable to fine and prosecution u/s. 629, 2) Any person who does not comply with the requirements of Sec. 209A shall be liable for fine and imprisonment u/s.209A(8) and 3) A Director who is convicted of an offence under the above sections shall be deemed to have vacated his office forthwith and shall be disqualified from holding such office in any company for the next 5 years as provided u/s. 209A(9).

WIRC Advertisements & Announcements

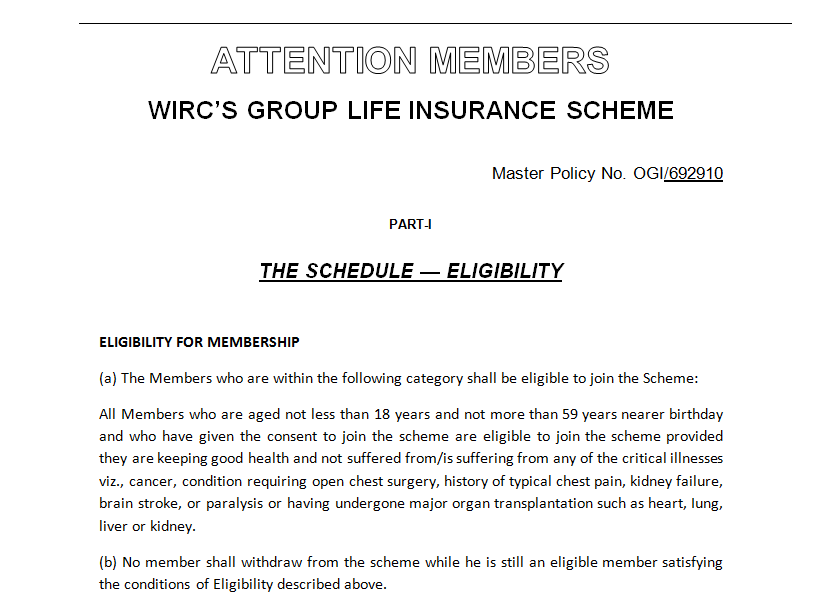

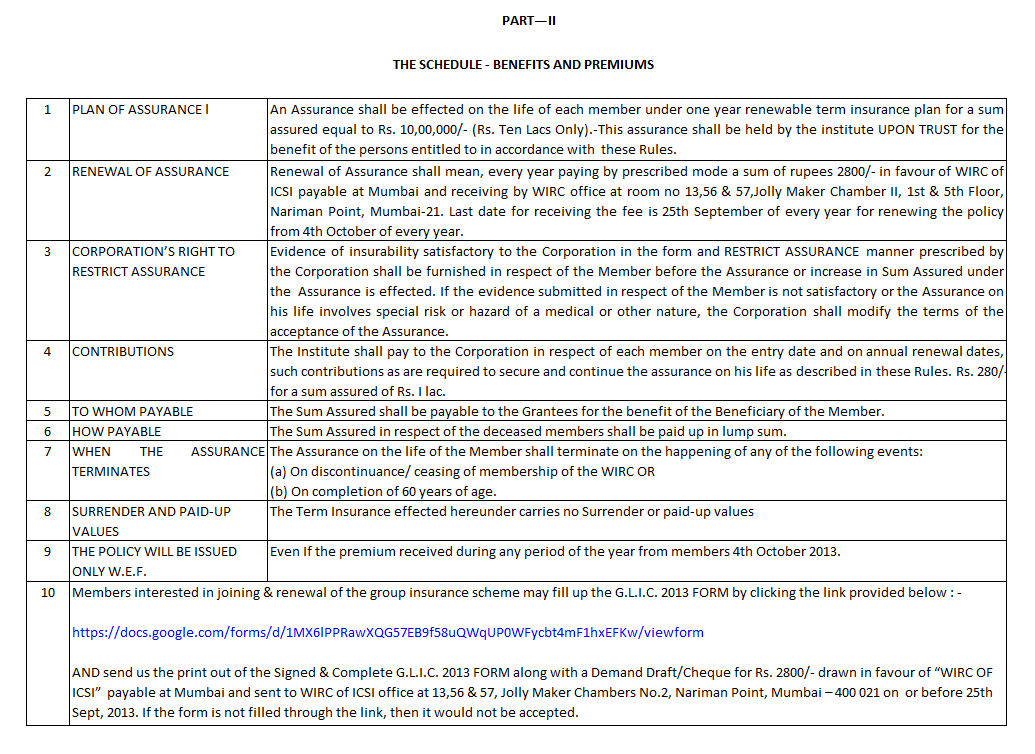

GLIC ANNOUNCEMENT

GLIC ANNOUNCEMENT

16th August 2013

Dear Member,

Sub: - WIRC’S GROUP INSURANCE SCHEME

The above scheme was introduced for the benefit of members with effect from 01st October, 2006 and many members from the Region are enrolled as members of the scheme.

The salient features of the scheme are stated below: -

1. Rs.10 lakh term cover per individual member.

2. The cover is global.

3. Premium payable is Rs.2,800/- per annum.

4. A member hailing from Western Region is eligible to become member of the scheme.

5. No health checkup is required, but a simple declaration of good health is essential.

6. Age limit- Not more than 59 years.

The above scheme is due for renewal on 1st October, 2013 and therefore the consolidated premium due has to be remitted by WIRC to the L.I.C., the Insurer by not later than Friday 27th September, 2013.

We therefore call upon to remit through Demand Draft OR Cheque a sum of Rs. 2800/- drawn in favour of “WIRC OF ICSI” payable at Mumbai and sent to WIRC of ICSI Office at 13,56 & 57, Jolly Maker Chambers No.2, Nariman Point, Mumbai – 400 021 on or before 25th September, 2013. Kindly mention your name and membership number on the back side of the Demand Draft OR Cheque.

A link has been provided for accessing G.L.I.C. 2013 FORM. It is essential to send us a print out of the Filled & Signed (Member and Witness) G.L.I.C. 2013 FORM along with the Demand Draft OR Cheque. Please note that simply sending the Demand Draft OR Cheque will not be considered unless accompanied by the Signed copy of the Filled G.L.I.C. 2013 FORM.

Thanking you.

Yours faithfully,

K C Kaushik

Assistant Director

Case Laws at a Glance

A Bird’s Eye View: Recent judgements on Company Law

1) COMPROMISE AND ARRANGEMENT

1) COMPROMISE AND ARRANGEMENT

Applicant-directors of company-in-liquidation submitted scheme of revival of company-in-liquidation. Single Judge declined sanction to such scheme. Applicant preferred appeal whereby Division Bench by interim order directed to implement scheme pending appeal. However, later on de novo consideration of scheme Division Bench passed an order dated 07.10.2011. Appellant sought review of that order on ground that no approval was obtained from company court for engagement of counsel appearing for Official Liquidator. Merely because advocate was lacking authority, per se, was no ground to review and recall order, more particularly when it was not found that any action was taken by OL or by advocate engaged by OL against interest of company-in-liquidation for opposing appeal preferred by applicant. Thus, no valid ground was made to recall or review order, dated 07.10.2011.

– RAJEEV S. MARDIA AND RASIK S. MARDIA V. OFFICIAL LIQUIDATOR OF MARDIA STEEL LTD. [2013] 118 SCL 77 (GUJRAT)

2) MEETINGS AND PROCEEDINGS

Notice sought to be published/circulated or reading out at general meeting in fact is a mere abuse of process of law to secure needless publicity for defamatory matter, same cannot be allowed. Respondents had dispute in respect of allotment of shares in HDFC-CLB exempted HDFC from publishing, circulating or reading notice proposing removal of HDFC’s chairman and director. Respondents acquired very insignificant number of shares in Petitioner Company and sought to publish/read out notice at general meeting proposing to remove its shareholder director who was also MD of HDFC. Respondents had not come with clean hands and, thus, Petitioner company was to be exempted from publication, circulation or reading out the notice at forthcoming general meeting.

- BSE LIMITED V. SURESHCHANDRA V. PAREKH AND MS. NLLABEN S. PAREKH [2013] 118 SCL 203 (CLB- MUMBAI)

3) CIRCUMSTANCES IN WHICH A COMPANY MAY BE WOUND UP

Petitioner-company had supplied certain goods to Respondent-company but value had not been paid to it. Respondent failed to make payment and made false promises. Petitioner issued statutory notice under section 434. Respondent filed a memo and gave cheques to Petitioner in settlement but same got dishonoured. Petitioner sought for restoration of winding up Petition. Respondent itself admitted debt but failed to pay same and, therefore, it was ordered to be wound up.

- AAKARSH INDUSTRIES (P.) LIMITED V. SHAKAMBARI FASHIONS (P.) LIMITED [2013] 117 SCL 116 (KAR.) (MAG.)

4) COMPANY COURT

Common law right under the memorandum of understanding can be enforced in ordinary civil courts by shareholders. – Sections 2(11) and 10 read with section 9 of Code of Civil Procedure, 1908

– K SARAVANAN V. COSMOPOLIS PROPERTIES (P.) LTD. [2013] 113 CLA 199 (MAD.)

5) RECTIFICATION OF REGISTER OF MEMBERS

Company Law Board would be justified in directing the company to rectify register of members in the absence of original documents – Sections 111 and 111A

– UNIT TRUST OF INDIA V. JAGAN NATH SAYAL & CO. [2013] 113 CLA 214 (DEL)

6) OPPRESSION / MISMANAGEMENT

Ad interim injunction cannot be granted to the Petitioners who fail to establish a prima facie case of oppression/mismanagement in their favour. – Sections 397, 398, 111, 402 and 403

– REACON ENGINEERS (INDIA) (P.) LTD. V. VENKATESWAR MEDICARE (P.) LTD. [2013] 113 CLA 272 (CLB)

7) OFFENCE PUNISHABLE UNDER SECTION 211(7)

The Company Law Board has the jurisdiction to compound an offence other than offence punishable with imprisonment only or imprisonment and also with fine – Section 621A read with section 211(7)

– V L S FINANCE LTD. V. UNION OF INDIA [2013] 114 CLA 300 (SC)

8) CERTIFICATE OF SHARES

The Company Law Board has power to pass order directing the company to deliver to the Petitioners certificates of shares allotted to them – Section 113

– DIPIKA M SHAH V. JAI PRAKASH ASSOCIATES LTD. [2013] 114 CLA 403 (CLB)

Circulars & Notifications

MINISTRY OF CORPORATE AFFAIRS

MINISTRY OF CORPORATE AFFAIRS

1. POWER OF ROCs TO OBTAIN DECLARATION/AFFIDAVITS FROM SUBSCRIBERS/FIRST DIRECTORS AT THE TIME OF INCORPORATION

General Circular No. 11/2013

Source: www.mca.gov.in

The matter of protection of interest of investors, including depositors, is very important to ensure healthy corporate capital market environment in the country. The recent instances of raising of monies by companies in a manner which is opaque/convoluted, non-accountable and which does not protect interests of depositors have been taken note of by the Ministry seriously.

Keeping in view the need to protect the interest of investors and ensure that companies raise monies in accordance with the provisions of the Companies Act/Deposit Rules, it is clarified that in exercise of the powers under the Companies Act, the Registrar of Companies may obtain declaration/affidavits from subscribers/first directors first at the time of incorporation and from directors, subsequently whenever company changes its objects, to the effect that company/directors shall not accept deposits unless compliance with the applicable provisions of Companies Act, 1956, RBI Act, 1934 and SEBI Act, 1992 and rules/directions/regulations made there under are duly complied and filed with the concerned authorities.

2. NAME AVAILABILITY GUIDELINES, 2011 — REGISTRATION OF ELECTORAL TRUSTS AS COMPANIES UNDER SECTION 25 OF THE COMPANIES ACT, 1956.

2. NAME AVAILABILITY GUIDELINES, 2011 — REGISTRATION OF ELECTORAL TRUSTS AS COMPANIES UNDER SECTION 25 OF THE COMPANIES ACT, 1956.

General Circular No. 12/2013

Source: www.mca.gov.in

In continuation to this Ministry's circulars no. 45 dated 8.7.2011, 48/2011 dated 22.07.2011 and 7/2012 dated 25.04.2012 on the subject cited above and to say that in para no.9 (iii) of General Circular No.45 dated 08.07.2011 is modified as under:-

"(iii) If it includes the words indicative of a separate type of business constitution or legal person or any connotation thereof, the same shall not be allowed For e.g: Cooperative, sehkari, trust, LLP, Partnership, Society, proprietor, HUF, Firm, Inc., PLC, GmbH, SA, PTE, Sdn, AG etc

Explanation:

1. Name including phrase 'Electoral Trust' may be allowed for Registration of companies to be formed under section 25 of the Companies Act, 1956 under the Electoral Trusts Scheme, 2013 as notified by the Central Board of Direct Taxes (CBDT).-

2. However, the company to be formed under section 25 of the Act, shall be the new company and such company will be required to comply with section 293-A of the Act. Further, Name application may be accompanied with an affidavit to the effect that the name to be obtained shall be only for the purpose of registration of companies under Electoral Trust Scheme as notified by the CBDT.

3. This issues with the approval of competent authority.

CUSTOMS

1. REGARDING INTRODUCTION OF RISK MANAGEMENT SYSTEMS (RMS) IN EXPORTS

Circular No. 23/2013 – Customs

Source: www.cbec.gov.in

1. Attention is invited to the Board Circular No.43/2005-Cus dated 24.11.2005 whereby Risk Management System (RMS) was introduced in Imports as a trade facilitation measure and for selective interdiction of high risk consignments for Customs control.

2. Implementation of RMS in Imports has been one of the most significant steps in the ongoing Business Process Re-engineering initiative of the department. In continuation of this initiative, the Board has now decided to introduce RMS in exports in Customs locations where the Indian Customs EDI Systems (ICES) is operational. The RMS in exports will enable low risk consignments to be cleared based on self assessment of the declarations by exporters. This will enable the department to enhance the level of facilitation and speed up the process of cargo clearance. By expediting the clearance of compliant export cargo, the RMS for exports will contribute to reduction in dwell time, thereby achieving the desired objective of reducing the transaction cost in order to make the business internationally competitive. The RMS in Exports is scheduled for implementation from 15.07.2013 onwards.

3. The RMS for exports is developed with the following components (i) ensuring appropriate control measures for proper and speedy disbursement of drawback and other export incentives (ii) effective utilization of human resources, to match the workload with the resources available (iii) ensuring proper and expeditious implementation of existing control over export under the applicable Allied Acts and Rules.

4 With the introduction of the RMS in exports, the present practice of routine verification of self-assessment and examination of Shipping Bills will be discontinued and the focus will be on quality assessment, examination and post clearance audit (PCA) of Shipping Bills selected by the Risk Management System.

5. Shipping Bills filed electronically into ICES through the Service Centre or the ICEGATE will be processed by RMS. The RMS will process the data through a series of steps/corridors and produce an electronic output for the ICES. This output from RMS will determine the flow of the Shipping Bill in ICES i.e. whether the Shipping Bill will be taken up for Customs control (verification of self-assessment or examination or both) or to be given “Let Export Order” directly after payment of Export duty (if any) without any verification of self-assessment or examination. The RMS will also provide instructions for Appraising Officer/Superintendent, Examining Officer/Inspector or the Let Export Order (LEO) Officer, wherever necessary. The decisions communicated by the RMS on the need for verification of self-assessment and/or examination and the appraising and examination instructions communicated by the RMS have be followed by the field formations. It is possible that in a few cases, the field formations might decide to apply a particular treatment to the Shipping Bill which is at variance with the instructions received for the RMS owing to risks which are not factored in the RMS. Such a course of action shall however be taken only with the prior approval of the jurisdictional Commissioner of Customs or an officer authorised by him for this purpose, who shall not be below the rank of Addl./Joint Commissioner of Customs, and after recording the reason for the same. A brief remark on the reasons and particulars of Commissioner’s authorization should be made by the officer examining the goods in the departmental comments in the EDI system.

6. Board has decided to implement RMS in export in two phases. In the first phase the RMS will process the data and provide the output to ICES only up to goods examination stage. In the second phase, the RMS will also process the Shipping Bill data after the Export general Manifest (EGM) is filed electronically and provide output to ICES for selection of shipping Bills for Drawback scrutiny and Post Clearance Audit (PCA).

7. With the implementation of export RMS, a Post Clearance Audit (PCA) function will be introduced in respect of exports after the LEO is given for export consignment. The objective of PCA is to monitor, maintain and enhance compliance levels, while reducing the dwell time of cargo. The RMS will select the Shipping Bills for audit, after issue of LEO, and these selected Shipping Bills will be directed to the audit officers for scrutiny by the ICES. It may be noted that the auditors are specifically being instructed to scrutinize declarations with reference to exports incentives, duty drawback and other compliance requirements wherever necessary, RMS will provide instructions for audit Officers. In case any possible short levies or undue claim of export incentives are noticed, the officer will issue a Consultative Letter setting out the ground for their views to the exporters/CHAs. Audit Officers should also scrutinize declarations with reference to data quality and advise the exporters/ CHAs suitably where the quality of their declarations is found deficient. Such advice is expected to be followed and will be monitored by the Local Risk Managers (LRM).

8 As in the case of Import, the national management of the Risk Management systems shall be the responsibility of the Risk Management Division. There will be a single Local Risk Manager (Admin) for a location for both import and export.

9. The implementation of RMS for exports will necessitate reorganization for staff. Board desires the Chief Commissioner of Customs to undertake a comprehensive re- organization of the officers deployed for processing of Shipping Bills. The present appraising facilities should be right-sized in tune with the quantum of Shipping Bills coming for assessment. A separate PCA section needs to be created and sufficient staff should be diverted to the Post Clearance Audit. The strength of the staff for examination of cargo would also be required to be readjusted.

10. With the introduction of RMS in exports, the selection of Shipping Bills for verification of Self-assessment and/or examination will be based on the output given by RMS to ICES. Accordingly the examination and assessment norms contained in the Board’s Circulars No. 06/2002 –Cus dated 23.01.2002, 01/2009-Cus dated 13.01.2009 and 28/2012-Customs dated 16.11.2012 would stand modified to that extent. However, owing to some technical reasons if the RMS fails to provide output to ICES or RMS output is not received at ICES end in time, the existing norms of assessment and examination prescribed by the aforementioned circulars will be applicable.

11. To begin with, RMS in Exports will be introduced w.e.f. 15.7.2013 at ICD Mulund and ICD Patparganj. With the implementation of RMS in exports the existing facilitation scheme viz. Accelerated Clearance System vide Circular No.30/2003-Cus dated 4.4.2003. would be phased out. As the deployment of the export RMS is likely to take place in a phased manner across the ICES locations, the existing facilitation scheme will continue to be operative in each Customs station until the operationalisation of the export RMS at the station.

12. Board desires DG (Systems) to forward the detailed instruction/draft public notice to field formation separately.

13. Any difficulty in implementation of these instructions should be brought notice of the Board immediately.

2. REGARDING CLASSIFICATION OF ELEMENTS OF FILTERS OF HEADING 8421

Circular No. 24/2013 – Customs

Source: www.cbec.gov.in

1. The Board has noted that while majority of import data in National Import Data Base shows that “elements of Filters” are being classified under Tariff Item 84219900 as parts of Filters. These articles are also being classified under other Tariff Items viz. 39269099, 48120000, 48239090, 59119090, 68159990, 69091910, 73269099, etc. Therefore, Board has examined the matter with a view to provide clarity in classification of said articles under the Customs Tariff Act, 1975.

2. Heading 8421 of the Customs Tariff applies to, “Centrifuges, including centrifugal dryers; filtering or purifying machinery and apparatus, for liquids or gases”. The scope of parts of articles covered by the said Heading 8421 is explained in the World Customs Organization’s Harmonized Commodity Description and Coding System Explanatory Notes. These Explanatory Notes present an internationally accepted view of the scope of each Heading of the Customs Tariff. In this context, the Explanatory Note to Heading 84.21 provides that:

“Subject to the general provisions regarding the classification of parts (see the General Explanatory Note to Section XVI), the heading covers parts for the above-mentioned types of filters and purifiers. Such parts include, inter alia:

Leaves for intermittent vacuum filters; chassis, frames and plates for filter presses; rotary drums for liquid or gas filters; baffles and perforated plates, for gas filters.

It should be noted, however, that filter blocks of paper pulp fall in heading 48.12 and that many other filtering elements (ceramics, textiles, felts, etc.) are classified according to their constituent material.” (Emphasis provided)