ICSI - WIRC FOCUS

Vol. XXX • No. 15 •Mar 2014

Chairman’s Blog

Dear friends

Dear friends

“As long as you’ve got passion, faith, and are willing to work hard, you can do anything and have anything you want in this world.”

As we are on the verge of being party of history with the introduction of the Companies Act, 2013 (new act) this phase in our life while

providing us with opportunities also calls for us to be ready with challenges which are being thrown up under the new act.

As you are aware that the notified rules have thrown at us a different kind of challenge wherein there were deviation from the draft rules.

The members of the ICSI though out the country drew the attention of the Law makers of these major lapse. We the CS professionals on whom

the responsibility for successful implementation of the new act lays have acted with responsibility and the Council members have left no

stone unturned for protecting the interests of the members not only for the purpose of employment but also because we are the trustees under

the new act for better governance and compliance.

Visions and value enhances the financial performance of an organization. Knowledge value ideas & vision form the inner core of organisation

that describes our mission, vision and values. Our efforts are always on as from last three months from January to March every Saturday we

had professional development programme. We will have series of companies act programmes. We are successfully running study circle at our

WIRC office, Andheri, Kandivali, Borivali and Ghatkopar.

I request all the members to become member of our professional development programme .I appeal to all the members to become member of our

benevolent fund.

At last but not the least call upon you to actively participate in the various ICSI initiatives and contact me directly for your suggestions,

inputs, feedback and grievances.

Let’s have Mission, Knowledge, Vision and Value.

Editorial Board

Photo Feature

RBI finally amends FEMA regulations to permit FDI in LLPs

Preamble

Preamble

While Limited Liability Partnership Act, 2008 permitted person resident outside India to become a partner in the Limited Liability Partnership (LLP), Foreign Direct investment(FDI) was not permitted under the Foreign Exchange Management Ac,1999 and rules and regulations issued thereunder.

The Cabinet Committee on Economic Affairs (CCEA) on 11th May, 2011 had approved the proposal to amend the FDI policy on allowing FDI in LLP and implement the same in a regulated manner by beginning with ‘open’ sectors where monitoring is not required. Thereafter, Ministry of Commerce and Industry, Department of Policy and Promotion (DIPP) reviewed the Consolidated FDI Policy for allowing FDI in LLP and made amendments therein vide Press Note No.1 (2011 Series) dated 20th May, 2011 which became effective from 1st April, 2011.LLPs were permitted to raise FDI only after obtaining FIPB approval. LLPs engaged in Sectors where a) 100 % FDI is permitted under the automatic route and b) no FDI- linked performance related conditions were imposed under the FDI policy.

Further, LLPs with FDI were subject to other conditions viz. a) not to operate in agricultural/plantation activity, print media or real estate business; b) not eligible to make any downstream investments; c) should be only for cash consideration and inward remittance should be through normal banking channels or by debit to NRS/ FCNR account of the person concerned, maintained with AD bank; and d) not permitted to avail External Commercial Borrowings.

However, Reserve Bank of India (RBI) had not amended the FEMA (Transfer or Issue of Security by a person resident outside India) Regulations, 2000 (the Regulations) in order to effect the amendment allowing LLPs to accept FDI.

Retrospective Amendment in FEMA regulations by RBI

The long wait got over on 13th March, 2014 when RBI carried out the necessary amendments by way of FEMA (Transfer & Issue of Security by a person resident outside India) (Third Amendment) Regulations, 2014. The Gazette copy of the Notification is enclosed as Annexure A. The amendment shall be deemed to have been come into force from 20th May, 2011

Regulation 2, dealing with definitions, was amended by way of insertion of definition of LLP to the following effect:

“(viiA) ‘Limited Liability Partnership (LLP)’ means a partnership formed and registered under the Limited Liability Partnership Act, 2008”

Further, Regulation 5 which dealt with “Permission for purchase of shares by certain persons resident outside India” was amended to insert a sub-regulation to the following effect:

“9. A person resident outside India (other than a citizen of Pakistan or Bangladesh) or an entity incorporated outside India, (other than an entity in Pakistan or Bangladesh), not being a registered Foreign Institutional Investor or Foreign Venture Capital Investor or Qualified Foreign Investor registered with SEBI or Foreign Portfolio Investor registered in accordance with SEBI guidelines, may contribute foreign capital either by way of capital contribution or by way of acquisition/transfer of profit shares in the capital structure of an LLP under Foreign Direct Investment, subject to the terms and conditions as specified in Schedule 9”

Schedule 9 deals with “Scheme for Acquisition/Transfer by a person resident outside India of capital contribution or profit share of Limited Liability Partnerships (LLPs)” which inter alia specifies conditios with respect to LLPs that can accept FDI, investors, investment, mode of payment etc. discussed in detail hereunder.

Who can invest?

Having gained a brief idea on the captioned subject, the next question which strikes is the clarity on the eligible investors. As one can ascertain from plain reading of sub-regulation 9 of Regulation 5 of the Regulations, an eligible investor shall be a person resident outside India or an entity incorporated outside India except any citizen/entity of Pakistan and Bangladesh; SEBI registered FIIs/ FVCIs/ QFI / FPIs .

Which LLPs can accept FDI?

In the above backdrop, we now need to reflect on who can appropriately be referred to as an eligible LLP. RBI has notified to include only those LLP’s which operate in open sectors/ activities i.e. where 100% FDI is allowed through the automatic route . This includes sector/activity viz. mining, petroleum and natural gas , Airports (Greenfield projects), Courier services, Industrial Parks, Trading, E-commerce activities, Pharmaceuticals (greenfield), Civil Aviation sector- Maintenance and Repair organizations; flying training institutes; and technical training institutions.

Moreover a restriction list has been added in respect of those LLP’s which cannot receive FDI namely:

• Sectors eligible to accept 100% FDI under automatic route but are subject to “FDI-linked performance related conditions.” By the term “FDI- linked performance related conditions” we mean those sectors where certain stipulated conditions are prescribed. (For example minimum capitalisation norms applicable to 'Non- Banking Finance Companies' or 'Construction Development: Townships, Housing, Built-up infrastructure);

• Sectors eligible to accept less than 100% FDI under automatic route- Petroleum refining by the Public Sector Undertakings (PSU), Cable Network etc.

• Sectors eligible to accept FDI under Government Approval route- Tea plantation; mining and mineral separation of titanium bearing minerals and ores, Defence, Broadcasting content services, Air transport services, satellite- Establishment and operation, Private Security Agencies, Multi Brand retail trading etc.

• LLP’s operating in agricultural, plantation activity and print media;

• The sectors which are restricted with FDI caps;

• The prohibited sectors under extant FDI Policy - Lottery Business, Gambling and Betting, Chit funds, Trading in Transferable Development Rights (TDRs) etc.

Whether under Automatic or approval route ?

Any form of foreign investment in a LLP whether direct/indirect shall be allowed only after obtaining the prior approval of the Foreign Investment and Promotion Board (FIPB).

At what price?

A LLP can receive FDI either by way of capital contribution or by way of acquisition/transfer of profit shares at more than or equal to Fair Price. Valuation certificate needs to be obtained from any Chartered Accountant or a practicing Cost Accountant or by approved valuer from the panel maintained by Central Government.

How is the payment to be made?

By way of cash consideration- through the normal banking channels by way of an inward remittance or by debit of the amount to (NRE) Account or FCNR (B) Account of the concerned person with AD Bank.

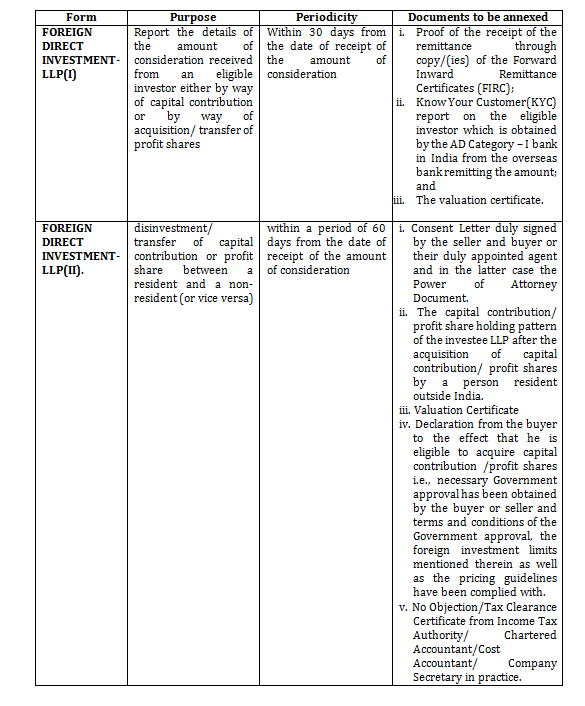

Reporting to be made to Regional Office of RBI in what form?

LLP which have received foreign investment between May 20, 2011 to the date of issuance of instructions issued in this regard by Reserve Bank shall comply with the reporting requirement in respect of FDI within 30 or 60 days, as applicable, from the date of issuance of these instructions

Downstream Investment in and by a LLP

An Indian Company having FDI (direct or indirect, irrespective of % of such investment) can make downstream investment in an LLP only if both, the Company as well as the LLP are operating in Sectors where a) 100 % FDI is permitted under the automatic route and b) no FDI- linked performance related conditions were imposed under the FDI policy.

LLP with FDI cannot make any downstream investment in any entity.

Other conditions

In case the designated partners of a LLP with FDI is a body corporate or nominates an individual to act as a designated partner, such body corporate should only be a company registered in India under the provisions of Companies Act as applicable Designated partners shall be responsible for compliance of conditions specified and also liable for penalties imposed on the LLP for any contravention.

Conclusion

FDI is presently permitted in companies, partnership firms, sole proprietary concerns subject to specified conditions. It was essential for RBI to issue amendment notification permitting FDI in LLP considering the benefits of the LLP structure. LLPs are very popular globally because they offer tax advantages, lower cost of formation and easier exit options.

This is surely a welcome move. While LLP sector had some bit of FDI from May,2011 till date, however, the entities which were hesitant to invest funds owing to lack of clarity in regulations, will surely make most of this opportunity.

An Overview on Money Laundering

Money Laundering is one of the major crises faced by the today’s Indian economy and economy of every nation of the world. An attempt is made

through this article to throw some light on the concept of money laundering, its impact on the corporate world in India and Prevention of Money

laundering Act, 2002.

Money Laundering is one of the major crises faced by the today’s Indian economy and economy of every nation of the world. An attempt is made

through this article to throw some light on the concept of money laundering, its impact on the corporate world in India and Prevention of Money

laundering Act, 2002.

BRIEF OVERVIEW ON WHAT IS BLACK MONEY AND MONEY LAUNDERING:

BLACK MONEY refers to funds earned on the black market, on which income and other taxes have not been paid. The total amount of black money

deposited in foreign banks by Indians is unknown.

MONEY LAUNDERING is an act to conceal or disguise the identity of illegally obtained proceeds in such a manner that they appear to have

originated from legitimate sources. Some of the examples of Money-Laundering in the corporate world cover the instances relating to Shell

Companies, Foreign Investments, Corporate Mismanagement, Insider Trading and Bribery etc.

originated from legitimate sources. Some of the examples of Money-Laundering in the corporate world cover the instances relating to Shell

Companies, Foreign Investments, Corporate Mismanagement, Insider Trading and Bribery etc.

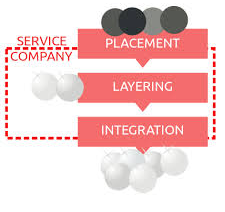

Money laundering is commonly defined as occurring in three steps:

• first step involves introducing cash into the financial system by some means ("placement");

• second involves carrying out complex financial transactions to cover-up the illegal source ("layering");

• Final step entails acquiring wealth generated from the transactions of the illegal funds ("integration").

Some of these steps may be omitted, depending on the circumstances; for example, non-cash proceeds that are already in the financial system would have no need for placement.

METHODS THROUGH WHICH A CORPORATES CAN ENGAGE INTO MONEY LAUNDERING:

• Structuring:

This is also known as smurfing. This is a method of placement whereby cash is broken into smaller deposits of money, used to defeat suspicion of money laundering and to avoid anti-money laundering reporting requirements. A sub-component of this is to use smaller amounts of cash to purchase bearer instruments, such as money orders, and then ultimately deposit those, again in small amounts.

• Bulk cash smuggling:

This involves physically smuggling cash to another jurisdiction and depositing it in a financial institution, such as an offshore bank, with greater bank secrecy or less rigorous money laundering enforcement.

• Cash-intensive businesses:

Under this method, a business typically involved in receiving cash uses its accounts to deposit both legitimate and criminally derived cash, claiming all of it as legitimate earnings. Service businesses are best suited to this method, as such businesses have no variable costs, and it is hard to detect discrepancies between revenues and costs.

• Trade-based laundering:

This involves under- or overvaluing invoices to disguise the movement of money.

• Round-tripping:

Here, money is deposited in a controlled foreign corporation offshore, preferably in a tax haven where minimal records are kept, and then shipped back as a foreign direct investment, exempt from taxation. A variant on this is to transfer money to a law firm or similar organization as funds on account of fees, then to cancel the retainer and, when the money is remitted, represent the sums received from the lawyers as a legacy under a will or proceeds of litigation.

• Real estate transactions:

Purchase of real estate with illegal proceeds and then sells the property. To outsiders, the proceeds from the sale look like legitimate income.

• Black salaries:

A company may have unregistered employees without a written contract and pay them cash salaries. Dirty money might be used to pay them.

Apart from the above said methods, there are some other methods of money laundering which are as follows:

• Financial Market Transactions;

• Out of Book Transactions;

• Manipulation of Books of Account, Expenses, Capital, Closing stock, Capital expenses etc.;

• Under-reporting of Production;

• Generation of Black money in Some Vulnerable Sections of the Economy;

• Investment through Innovative Derivative Instruments.

WHO SHALL BE HELD LIABLE FOR OFFENCES UNDER MONEY LAUNDERING IN THE CORPORATE WORLD?

Section 70 of the Prevention of Money Laundering Act, 2002 deals with the offences by Companies whereby it is clearly stated that;

Where a person committing a contravention of any of the provisions of this Act or of any Rule, Direction or Order made there under is a Company (company" means any body corporate and includes a firm or other association of individuals; and

• Every person who, at the time the contravention was committed, was

• in charge of, and

• was responsible to the company,

(i) for the conduct of the business of the company

(ii) as well as the company,

Shall be deemed to be guilty of the contravention and shall be liable to be proceeded against and punished the Act.

WHAT IS THE PUNISHMENT FOR MONEY LAUNDERING?

Person whoever commits the offence of money laundering shall be punishable:-

• With rigorous imprisonment for a term which shall not be less than three years but which may extend to seven / ten years or;

• Shall also be liable to fine which may extend to five lakh rupees.

PREVENTATIVE MEASURES TAKEN AGAINST MONEY LAUNDERING IN INDIA:

• PREVENTION OF MONEY LAUNDERING ACT, 2002 (PMLA):

Prevention of Money Laundering Act was enacted with effect from July 01, 2005. The Act forms the core of the legal framework to combat money laundering. This Act subserves a twin purpose to prevent money laundering and to provide for confiscation of property derived from, or involved in money laundering and to ensure curbing of the tendency of committing scheduled offences.

• RESERVE BANK OF INDIA (RBI) CONTRIBUTION:

Reserve Bank of India has also through it’s circulars from time to time issued guidelines on KYC/AML/CFT the objective of which is to prevent banks from being used, intentionally or unintentionally, by criminal elements for money laundering or terrorist financing activities.

KYC procedures also enable banks to know/understand their customers and their financial dealings better which in turn help them manage their risks prudently. Banks were advised to follow certain customer identification procedure for opening of accounts and monitoring transactions of a suspicious nature for the purpose of reporting it to appropriate authority. These ‘Know Your Customer’ guidelines have been revisited in the context of the Recommendations made by the Financial Action Task Force (FATF) on Anti Money Laundering (AML) standards and on Combating Financing of Terrorism (CFT).

The guidelines issued by the Reserve Bank are under Section 35A of Banking Regulation Act, 1949 (As Applicable to Co-operative Societies) and any contravention of or non- compliance with the same may attract penalties under the relevant provisions of the Act.

• SECURITIES AND EXCHANGE BOARD OF INDIA (SEBI) CONTRIBUTION:

SEBI has issued necessary directives vide circulars from time to time, covering issues related to Know Your Client (KYC) norms, Anti- Money Laundering (AML), Client Due Diligence (CDD) and Combating Financing of Terrorism (CFT).

SEBI Circular ISD/CIR/RR/AML/1/06 requires CSSIPL to collect certain information about each investor and verify their identity, supported by relevant identification documents. All investors, including persons appointed under a Delegation of Authority or Power of Attorney, are required to meet the KYC requirements under the PMLA laws and SEBI Circular ISD/CIR/RR/AML/1/06.

• OBLIGATIONS OF BANKING COMPANIES, FINANCIAL INSTITUTIONS AND INTERMEDIARIES:

Under Section 12 of Prevention Of Money Laundering Act, 2002 (PMLA), all Banking Companies, Financial Institutions And Intermediaries are required to maintain a record of all transactions, including information relating to transactions for a period of 5 years, in such manner as to enable it to reconstruct individual transactions, and furnish to the concerned Authorities under PMLA, all information relating to such transactions, whether attempted or executed; the nature and value of such transactions; verify the identity of its clients and the beneficial owner, if any; and maintain record of documents evidencing identity of its clients and beneficial owners as well as account files and business correspondence relating to its clients.

PREVENTATIVE MEASURES TAKEN AGAINST MONEY LAUNDERING WORLDWIDE:

• FINANCIAL ACTION TASK FORCE (FATF):

‘FATF’ was formed in 1989 by the G-7 countries i.e. United States, Japan, France, Germany, Italy, U.K. and Canada. The FATF is an intergovernmental body whose purpose is to develop and promote an international response to combat money laundering.

FATF is a policy-making body that brings together legal, financial, and law enforcement experts to achieve national legislation and regulatory AML and CFT reforms.

FATF has developed 40 recommendations on money laundering and 9 special recommendations regarding terrorist financing. FATF assesses each member country against these recommendations in published reports. Countries seen as not being sufficiently compliant with such recommendations are subjected to financial sanctions.

FATF’s three primary functions with regard to money laundering are:

I. Monitoring members’ progress in implementing anti-money laundering measures.

II. Reviewing and reporting on laundering trends, techniques, and countermeasures.

III. Promoting the adoption and implementation of FATF anti-money laundering standards globally.

• FINANCIAL TRANSACTION AND REPORTS ANALYSIS CENTRE OF CANADA (FINTRAC):

FINTRAC is responsible for investigation of money and terrorist financing cases that are originating from or destined for Canada.

• AUSTRALIAN TRANSACTION REPORTS AND ANALYSIS CENTRE (AUSTRAC):

AUSTRAC is Australia's anti-money laundering and counter-terrorism financing regulator and specialist financial intelligence unit.

Why so many legislations attract PMLA?

The endeavour of the Legislature is to cover not only the wealth earned through illegal means, but also to bring Illegal Income under the purview of PMLA, which includes even Legal Income that is concealed from public authorities. As per the White Paper of May, 2012 by the Ministry of Finance, Government of India, the Money-Laundering is not only the wealth earned through illegal means, the same would also include legal income that is concealed from public authorities:

• To evade payment of Taxes (Income Tax, Excise Duty, Sales Tax, Stamp Duty, etc);

• To evade payment of other statutory contributions;

• To evade compliance with the provisions of Industrial laws such as the Industrial Dispute Act 1947, Minimum Wages Act 1948, Payment of Bonus Act 1936, Factories Act 1948, and Contract Labour (Regulation and Abolition) Act 1970; and / or

• To evade compliance with other laws and administrative procedures.

The above itself clarifies, why PMLA has been amended to include a wide range of legalisations in India under its ambit, despite the fact that patently none of these legislations have anything to do with the definition of Money-Laundering, as of now any evasion of the state levies and dues will also tantamount to Money-Laundering and attract PMLA.

Punishment under PMLA

Section 4 of PMLA prescribes the Punishment for Money-Laundering as under:

• Rigorous Imprisonment for a term;

• which shall not be less than Three years, but

• which may extend to 7 years/10 years, and

• shall also be liable to fine.

The fine under PMLA is without any limit and the same may be commensurate to the nature and extent of offence committed and the money laundered.

CASE LAW:

SATYAM CASE:

Satyam Computers founder Ramalinga Raju and another accused appeared before a court in Hyderabad in connection with a prosecution complaint filed by Enforcement Directorate (ED) against them for offences under the Prevention of Money Laundering Act (PMLA),The Enforcement Directorate had file the complaint against Raju and 212 others, including 166 companies, before the XXI Additional Chief Metropolitan Magistrate Court cum Special Sessions Judge here for allegedly laundering funds under a “corporate veil” to perpetrate the accounting scam that rocked the business world in 2009. ED in its prosecution investigation report sought to “prosecute the accused for offence of money laundering” under PMLA. The court subsequently took cognizance of the complaint and had issued summons against the accused seeking their appearance. The ED report said that Ramalinga Raju and the other accused, who have also been probed by CBI, “derived proceeds of crime from the sale and pledge of inflated shares of M/s Satyam Computers and Services Ltd (SCSL)”.

The prosecution complaint (charge sheet), names 213 accused - 47 individuals (among them Ramalinga Raju and nine other accused already named in the CBI charge sheet in the multi-crore Satyam accounting fraud case) and 166 firms - including SCSL. Besides, Raju, the former chairman of Satyam Computers, his brother B Suryanarayana Raju, Satyam’s former MD B Rama Raju, ex-CFO Vadlamani Srinivas, former PwC auditors Subramani Gopalakrishnan, T Srinivas and Satyam’s former internal chief auditor V S Prabhakar Gupta were among others who appeared in the court and executed personal bonds of Rs 10,000 each.

ED which had earlier interrogated prime accused Ramalinga Raju, Rama Raju, and the others had registered a case against the Satyam founder and his family under PMLA, which defines money laundering offences as those involving money derived from any activity connected with the proceeds of crime. The Act provides for the freezing and seizure of the proceeds of crime. So far, 350 immovable and five movable properties, valued at a cumulative Rs 1,075 crore, have been attached in the case, ED had said.

ROLE OF COMPANY SECRETARY IN PREVENTING MONEY LAUNDERING:

The Company secretary is an officer in a ministerial and administrative capacity, who is charged with duty of ensuring that the affairs of the company are conducted according to the provision of companies act, Company secretary is also responsible for the efficient administration of a company, particularly with regard to ensuring compliance with statutory and regulatory requirements and for ensuring that decisions of the Board of Directors are implemented. Company secretary are responsible for ensuring that the business’s policies and procedures are designed and operate effectively to manage the risk of the business being used for financial crime and to fully meet the requirements of the Money Laundering Regulations 2007. Company secretary must produce adequate Anti- Money Laundering measures, risk management policies and risk profiles, including evidence of their policies. Company secretary will provide a framework of direction to the business and its staff and will identify named individuals and functions responsible for implementing particular aspects of the policy.

CONCLUSION:

Money laundering has many faces. It may cross borders through highly elaborate schemes, or it may be more rudimentary and restricted to a smaller area. The company intends to protect itself, but above all it wishes to provide assistance to its clients in this field, through staff training, advice on the creation and implementation of anti-money laundering procedures, advice on underwriting and involvement in monitoring claims.

Regime-Related Party & Related Party Transactions

Related Party Transactions (RPTs) had been always an important subject matter in and for preparation of financial statements of any company.

It has always been view by regulators that some advantage been passing to personal interest of the party having stake in the company.

Related Party Transactions (RPTs) had been always an important subject matter in and for preparation of financial statements of any company.

It has always been view by regulators that some advantage been passing to personal interest of the party having stake in the company.

The Companies Act, 1956 did not had any provisions covering aspects of related party, and or their transactions. However, only Accounting

Standard 18 (As-18) provides for disclosure norms to follow for preparation of financial statements.

The term “related party” and “related party transactions” prescribed in provisions of respective clause 2(76) and clause 188 of the new

Companies Act, 2013 have wider coverage. The following paragraphs explains the new provisions in context of the requirements, conditions,

consent, approval, disclosure, voidable and penalty along with identifying such transactions.

Further, the SEBI Board, also in its meeting held in New Delhi on February 13, 2014 inter-alia took the decisions to amend the listing agreement

with regards to RPTs more in line with the provisions of Companies Act, 2013. The important aspects which SEBI proposes to make it applicable to

all listed companies with effect from October 1, 2014. SEBI vide it circular dated April 17, 2014 had amended the Corporate Governance norms

namely clause 49 with regard to adopt best practice on governance in matter of related party transactions.

Under Clause 49, related parties include, besides covering the requirements of the Companies Act, 2013 and AS 18, additional relationships as

mentioned below;

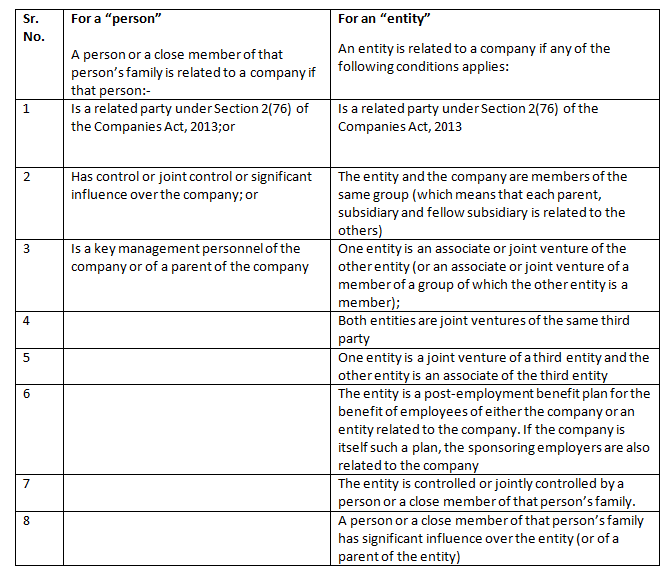

A ‘related party' is a “person” or “entity” that is related to the company.

In addition to the above party considered as related, the parties are also considered to be related if one party has the ability to control the

other party or exercise significant influence over the other party, directly or indirectly, in making financial and/or operating decisions.

The company shall formulate a policy on materiality of related party transactions and also on dealing with Related Party Transactions. The

transactions is material if the transaction/transactions to be entered into individually or taken together with previous transactions during

a financial year, exceeds the higher of i) 5% of the annual turnover or ii) 20% of the net worth of the company as per the last audited financial

statements of the company.

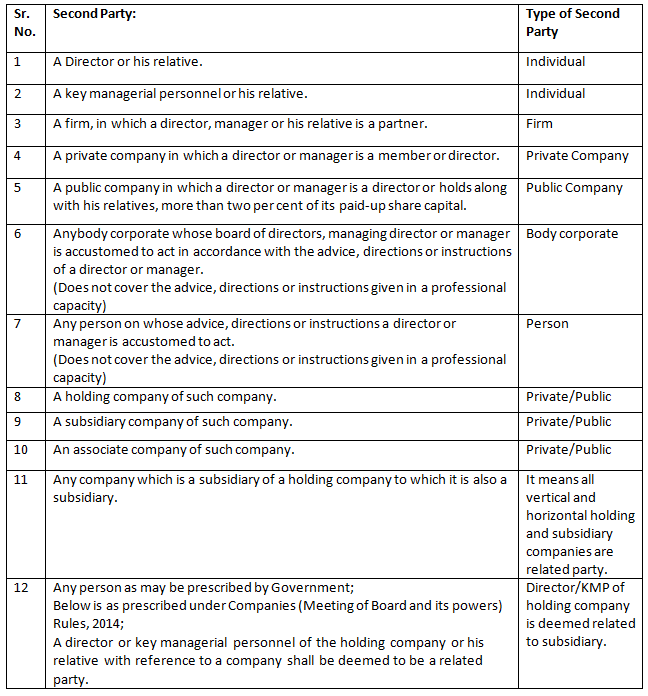

The term “related party’ under Companies Act, 2013 has been presented in simple format for the sake of simple understanding.

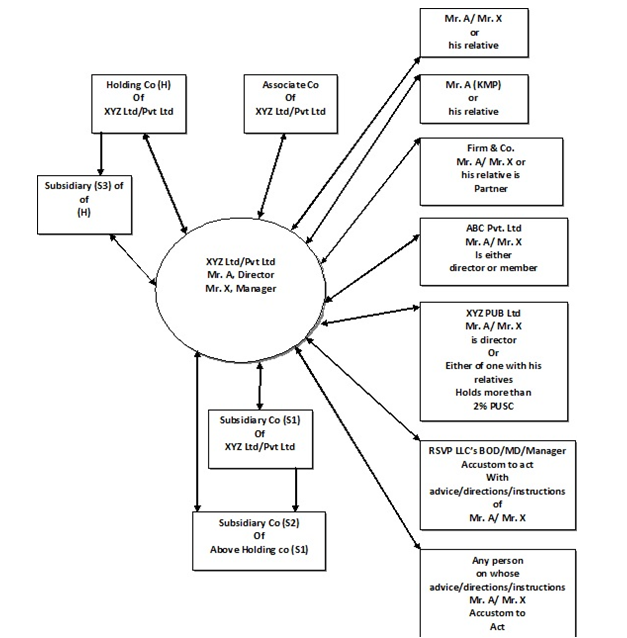

Company (be it public or private) as One Party enters transactions with any one of the entity as mentioned below as Second Party.

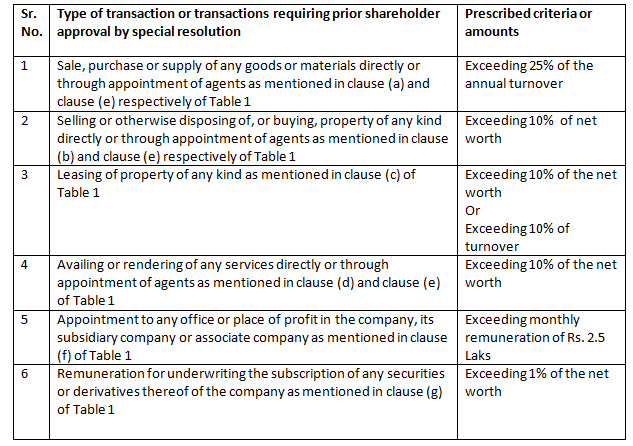

The following chart depicts the different related party covered under the new law;

“Double sided arrow shows the parties are “related”.”

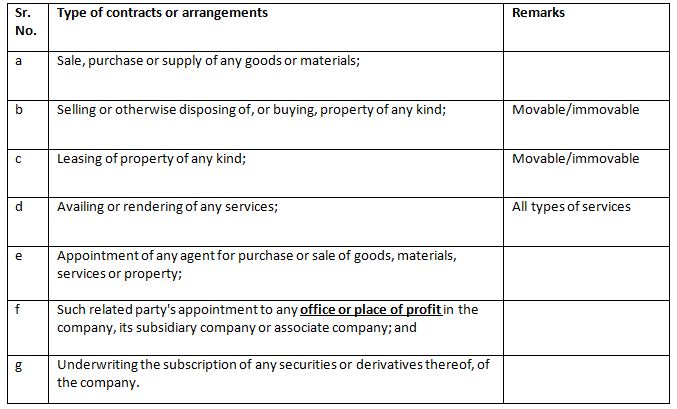

The following types of contract or arrangements are covered under the provisions of new law;

Office or Place of profit shall mean:

In case of a Director: Any office or place held by a Director and he receives some remuneration over and above the remuneration he is otherwise entitled to as a Director, by way of salary, fee, commission, perquisites, any rent-free accommodation, or otherwise.

In case of any other entity: Any office or place held by an individual other than a Director, or by any firm, Private Company or other Body Corporate, and such an entity receives from the company anything by way of remuneration, salary, fee, commission, perquisites, any rent-free accommodation, or otherwise

Requirements of the law:

I. Board consent in meeting

Consent of the board by resolution passed in its meeting is required, if the company enter into any contract or arrangement with a related party (RPT) with respect to the transactions mentioned in Table 1 above. Where any director is interested then such director shall not be present in the meeting during discussion of the matter of such contract or arrangement.

The company can enter into contracts or arrangements by passing resolution in its board meeting provided that the transactions does not cross limits mentioned in Table 2 and paid up share capital of the company is less than ten crore rupees.

II. Shareholders prior approval

Prior approval of the company by way of special resolution required where:-

a) Paid up share capital of the company is INR 10 Crore or more;

b) Transaction or transactions to be entered into as contracts or arrangements referred in Table 2 with prescribed criteria or amounts.

Accordingly, even if the company is not having a paid up share capital of Rs. 10 crore, but is entering into any of the transactions enumerated in Table 2, it has to pass a special resolution.

Also on the other hand, even if the company entering into any of the transactions not crossing the limits enumerated in Table 2, but paid up share capital is Rs. 10 crore or more, the company has to pass special resolution.

The Turnover or Net worth shall be on the basis of Audited Financial Statement of preceding Financial Year.

c) In case of listed company to follow below requirements also:

• Prior approval of Audit Committee for all RPTs.

• Approval of all material RPTs by shareholders through special resolution with related parties abstaining from voting.

• Policy on materiality of RPTs and also on dealing with RPTs.

d) In case of wholly owned subsidiary, the special resolution passed by the holding company shall be sufficient for the purpose of entering into the transactions between wholly owned subsidiary and holding company, i.e. the wholly owned subsidiary will not need to separately pass a special resolution.

III. Member not permitted to vote

If any member is related party then no such member can vote on special resolution to approve the contract/arrangement under consideration. Interested member need not to vote on special resolution to approve any contracts or arrangements required to be entered by the company. This requirement of law implies that disinterested minority shareholders can dictate the results of special resolution and may lead to a situation of impacting the business decision of the company.

To understand the practical difficulties as may be faced due to above requirements, for example company A in which 60% is held related parties. Now, if company A wants to enter into a transaction which is related party transaction and therefore by virtue of the provisions 60% majority are prohibited to vote in general meeting and the balance disinterested 40% shareholders should only vote. Since, approval by special resolution is required it means approval by only 30% of disinterested shareholders will be required. The situation may arise that any person holding 10% in company A could vote against the decision thus resulting into the total constraint in taking business decision, though could be good for the growth of the company, but merely by 10% minority shareholder, who may not have understood the transaction, which is good for the growth of the company A and as a result, despite promoters shareholders sincere and genuine efforts for the growth of company A may go in ruin.

IV. Disclosure requirements in the Board report and explanatory statement attached to notice to shareholders

• All related party transactions to be disclosed in board report with justification for entering into it. These disclosure requirements of law will increase more disclosure on transparency to the shareholders of the company.

• The explanatory statement annexed to the notice convening general meeting for obtaining shareholders approval must contain the following particulars, namely:-

1. name of the related party;

2. name of the director or key managerial personnel;

3. nature of relationship;

4. nature, material terms, monetary value and particulars of the contract or arrangement;

5. any other information relevant or important for the members to take a decision on the proposed resolution.

• For listed company:-

1. all material transactions with related party shall be disclosed, quarterly with compliance report on corporate governance; and

2. disclose the policy on the website of the company and also in its Annual Report.

V. Ratification

If contract entered without consent of board of prior approval of shareholders, as the case may be, the same can be ratified by the board or shareholder as the case may be within 3 months from date of entering it into.

VI. Provisions for Voidable contract/arrangement

The contract/arrangements if not so ratified in 3 months period then such contract or arrangement shall be voidable at the option of the Board.

VII. Indemnity against losses and recovery of any losses to/by the company

If the contract/ arrangement is with a party related to a director, or is authorized by another director, then the concerned directors shall indemnify the company against any losses incurred by it. Moreover now the law provides that company can proceeds against such directors or any other employee to recover any loss incurred by it due to such contract/arrangement entered in contravention of the law.

VIII. Penalty

To director or any other employee who authorized or entered such contract in contravention the penalty imposed is; in case of listed company imprisonment up to 1 year; or fine INR 25,000 may extend to INR 5, 00,000 or with both. In case of any other company fine INR 25,000 may extend to INR 5, 00,000

The question now here arises that are there any related party transactions which can be entered without attracting the provisions of the new Act. The Act, 2013 provides that nothing contained in Section 188 (1) shall apply to related party transactions which are in the ordinary course of business and on an arms’ length basis.

Therefore it is inferred that the transactions which are i) in ordinary course of business and are ii) at arm’s-length basis are permissible without attracting any of the conditions prescribed in the Act.

The new law explained the term “Arm’s length Transaction” which means a transaction between 2 related parties that is conducted as if they were unrelated, so that there is no conflict of interest.

The test for applicability of the provisions can be made by asking following 2 questions;

i) Is the contract is in ordinary course of business?

ii) Is the contract is at arm’s-length basis?

The provisions of new law will not get invoked if the answer to both questions is in affirmative.

Quantum jump in work for CS

-Compiled by Belgaum Study Circle

Amid the atmosphere of gloom and doom amongst CS fraternity that has set in after release of Rules under the Companies Act, 2013,which they

themselves eagerly awaited, there is silver lining to the dark clouds for all CS professionals, be they in service or practice, because,

henceforth board actions such as resolution to adopt draft balance sheet, resolution to borrow moneys, resolutions to make call on shares, make

investments, resolution to take note of disclosure of Directors interest, quarterly unaudited financial statements(for listed companies) need to

be filed with the Registrar of Companies, which was not prescribed in 1956 Act.

These board actions as well as the filings need to take place in a time bound manner, earlier too, time limit was prescribed but then, may be

because of relatively small quantum of additional fee and remote possibility of prosecution, both companies and CS took them lightly, as if

‘time was of no essence.’

However, henceforth these requirements as to filing which are in addition to the annual filings need to be taken seriously. The following Table

lists out number of compliances to be made, with different time limits and the quantum of penalty for violation which is staggering

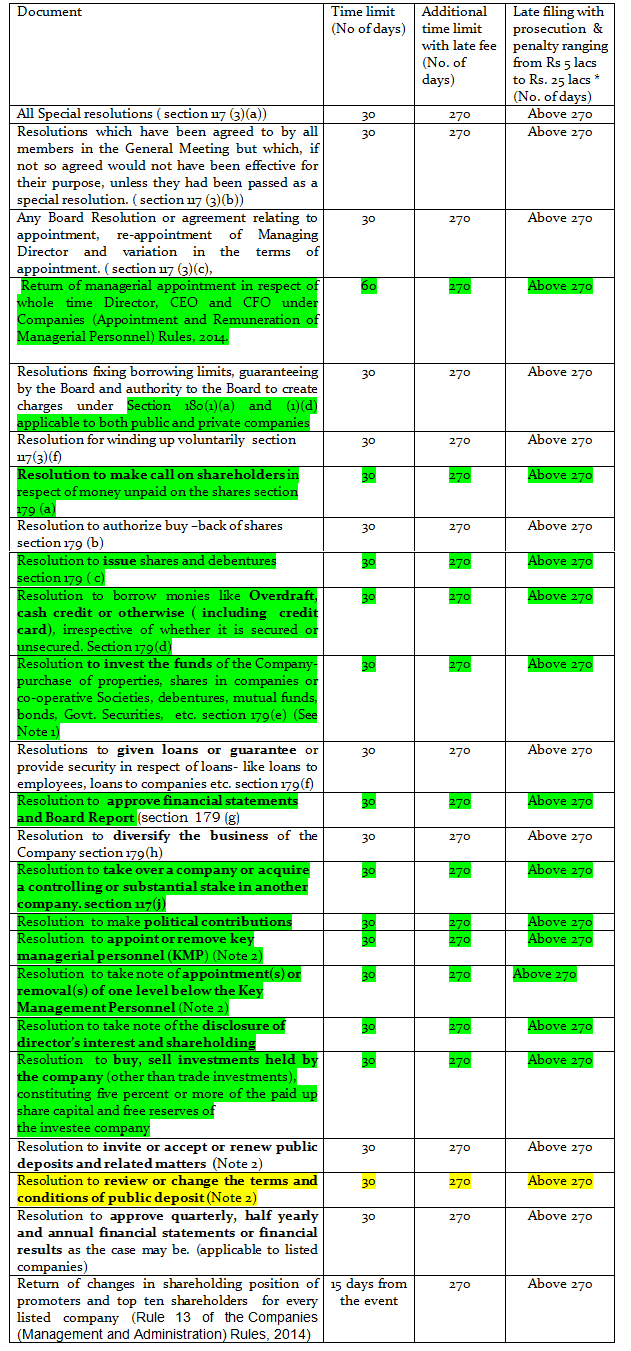

Resolutions and Agreements to be filed with Registrar of Companies (Sec. 117)

The documents mentioned below need to be filed with ROC, the new provisions are highlighted in green and yellow colour.

* In addition a penalty ranging from Rs. 1 lac to Rs. 5 lacs for officer in default.

Note 1: The investment shall be held in the name of the Company only.

Note 2: Not applicable to private companies.

Therefore, these compliances would provide succor to the CS profession and let us take the Rules as they are, as blessings in disguise,

instead of hankering after more and more certification work, which may in the end prove disastrous for the profession in view of the stiff

penalties that are prescribed on professionals for the mistakes, especially viewed in the context of the section 454 of the Companies Act,

2013 that empowers Government to appoint Adjudicatory Officers to try and penalize erring companies and the professionals, the earlier

scenario of ROC as a mere complainant before a Magistrate is now history, henceforth, the Departmental officer would not only act as the

complainant, but would be a judge and the executioner too. Of course right of appeal against an order of adjudicatory officer is provided,

and the proceedings may drag on forever, but then it is for us to decide as to what kind of practice one should do. Once appointed, the

adjudicatory officer would always be on a look out for his prey.

Another novel feature of the filing is the new provision contained in section 403of the Companies Act, 2013 which is similar to section 611 of

the 1956 but in the new Act there is a cut off period of 270 days from date of event to enable filing with additional fee. Belated filing

beyond 270 days from the date of event is also permitted but sub section 2 of section 403 holds out a threat of prosecution, so beyond 270

days delay, the company needs to pay additional fee and fine both.

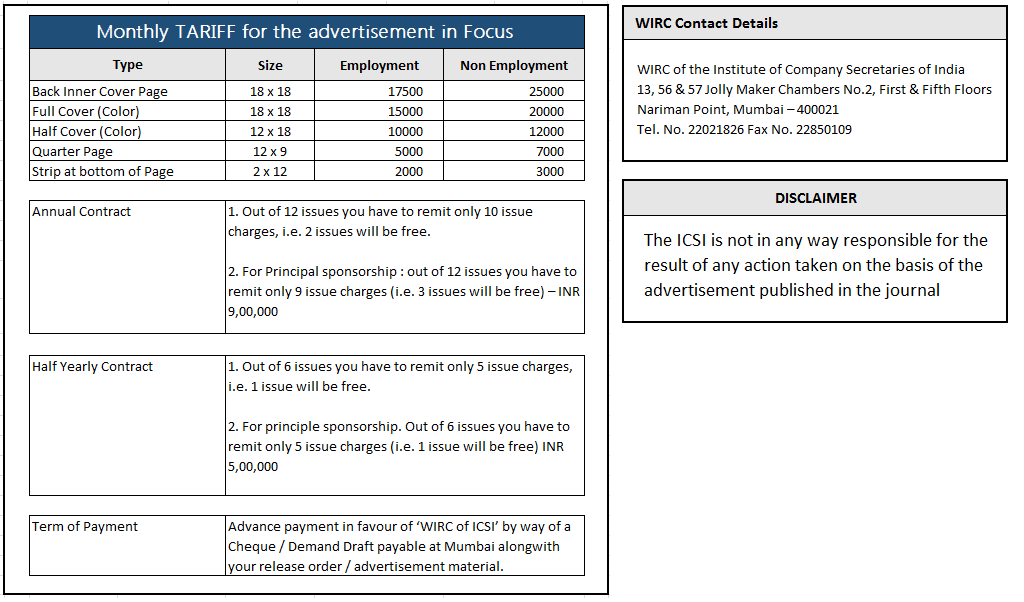

WIRC Advertisements/Announcements

Case Laws at a Glance

A Bird’s Eye View: Recent judgements on Company Law

1) COMPROMISE AND ARRANGEMENT

1) COMPROMISE AND ARRANGEMENT

A scheme of arrangement contemplating that a division of respondent-company would stand transferred to ‘Peter England’ was sanctioned by company Court on 1.3.2013. Appelent had entered into an agreement with respondent on 30.1.2007 purporting to create a sub-license in respect of certain premises in a mall at Kharagpur. Appellant had invoked arbitration and High Court directed respondents to furnish a bank guarantee of a nationalized bank of Rs. 6.50 crore. Single Judge by impugned order sanctioned scheme holding that claim of appellant had been secured by furnishing of a bank guarantee of Rs. 6.50 crores in terms of judgment of Calcutta High Court. Since claim of appellant was secured and appellant had not filed any affidavit setting out particulars of fraud despite of sufficient opportunity given to him, no interference in scheme already implemented was to be made. – LAXMI PAT SURANA V. PANTALOON RETAIL (INDIA) LTD. [2014] 124 SCL 62 [HIGH COURT - BOMBAY].

2) AMALGAMATION

Tenancy is a non-transferable object that could extend to others either by an explicit contract or by statute where order of amalgamation wasn’t served on landlord by transferee company and landlord continued to issue rent receipts in name of (dissolved) transferor company though he accepted rent from transferee company, no right of tenancy was created/transferred in favour of transferee company. – AMBALAL SARABHAI ENTERPRISES LTD. V. RAJEEV DAGA. [2014] 124 SCL 30 [HIGH COURT-CALCUTTA].

3) OPPRESSION AND MISMANAGEMENT

Petitioner is entitled to protection of section 14 of Limitation Act, 1963 where the Supreme Court dismissed appeals holding that the Company Law Board did not have the jurisdiction to pass its order – Sections 397 and 398 read with section 14 of Limitation Act, 1963. – WINSTAR INDIA INVESTMENT CO. LTD V. HALDIA PETROCHEMICALS LTD. [2014] 118 CLA 558 [HIGH COURT-CALCUTTA].

4) RECTIFICATION OF REGISTER

A person, who has not been allotted the shares and whose name is not entered in the register of members, has a right of appeal under sub-section (2) of section 111A - Section 111A (2). – UMESH KUMAR BAVEJA V. IL & FS TRANSPORTATION NETWORK LTD. [2014] 118 CLA 541 [HIGH COURT-DELHI].

5) WINDING UP

Official liquidator cannot approach the company court to set aside the auction or sale conducted by the Recovery Officer of Debts Recovery Tribunal. Section 457 read with section 20 of Recovery of Debts Due to Banks or Financial Institution Act, 1993. – OFFICIAL LIQUIDATOR, UP & UTTARAKHAND V. ALLAHABAD BANK [2013] 113 CLA 335 [SUPREME COURT].

6) CIRCULATION OF MEMBERS RESOLUTION

Company is entitled to be exempted from circulation of notice of member’s resolution being abuse of process of law to secure needless publicity for defamatory matter. Section 188 read with section 264. – B S E LTD. V. SURESHCHANDRA V PAREKH. [2013] 113 CLA 509 [CLB - MUMBAI].

Smile Please / Cartoon

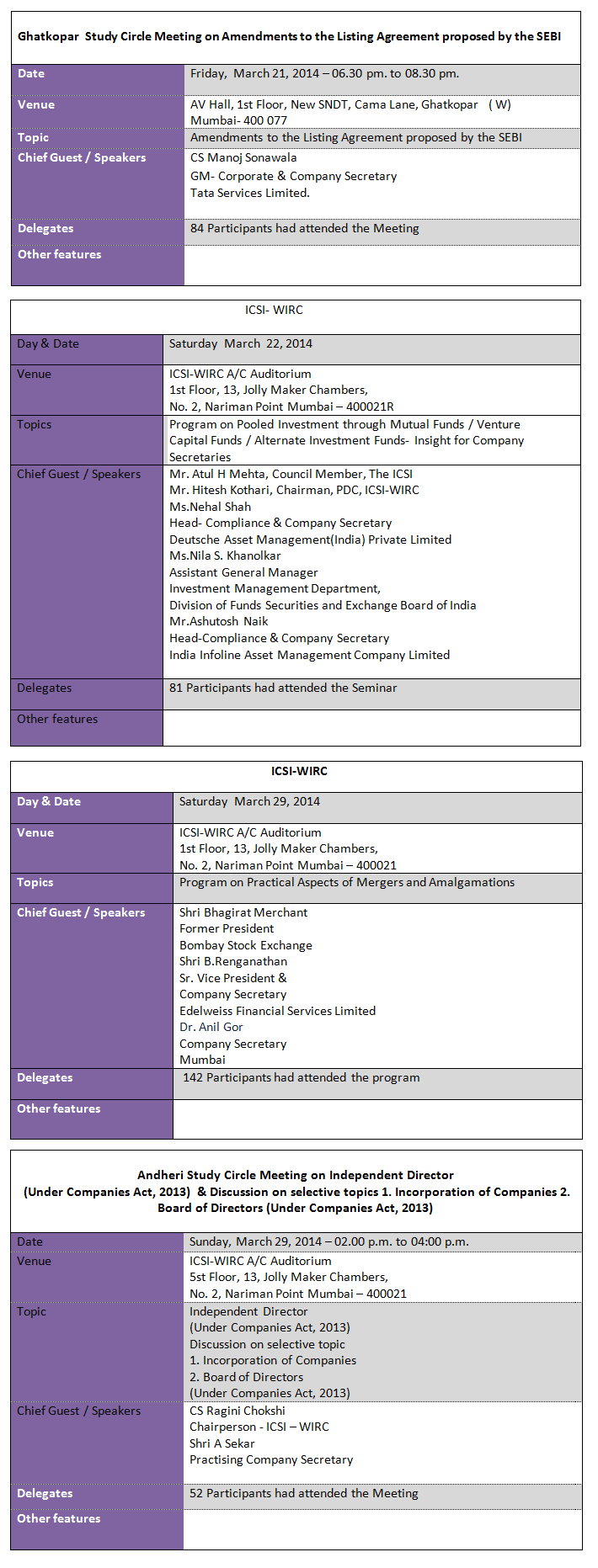

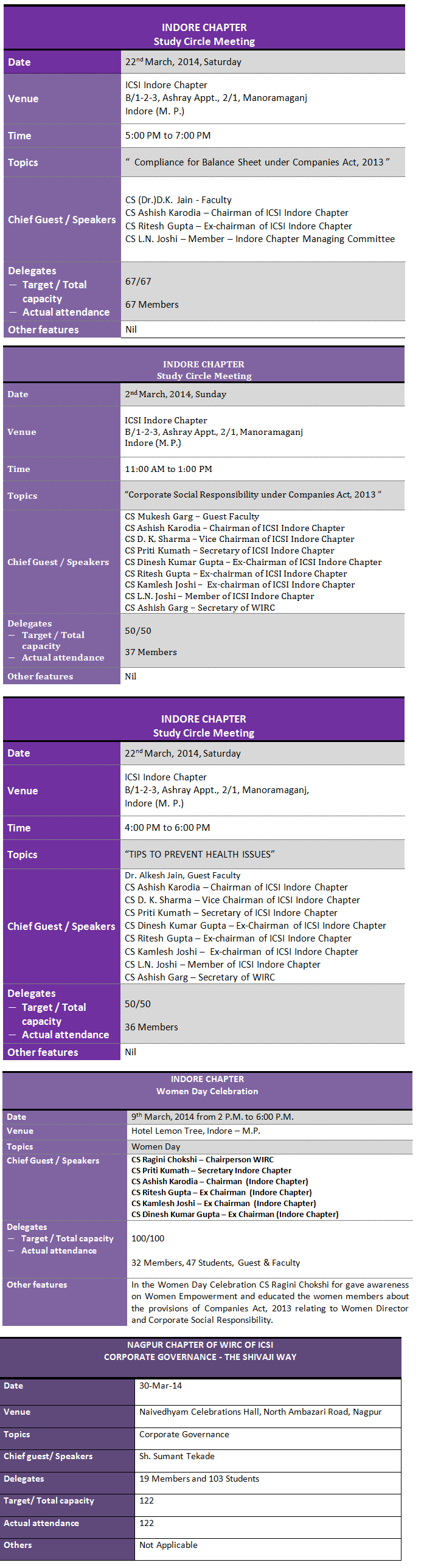

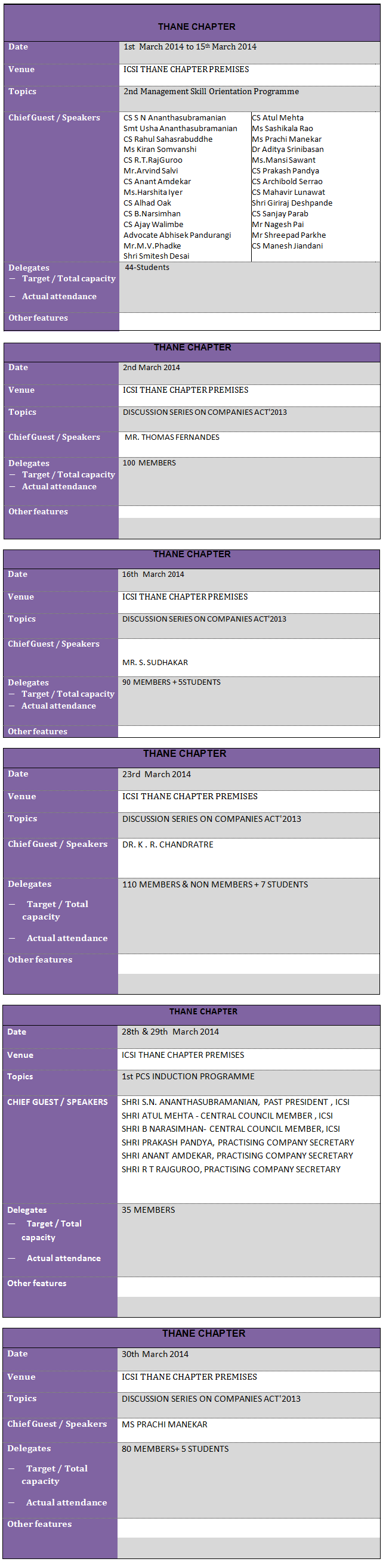

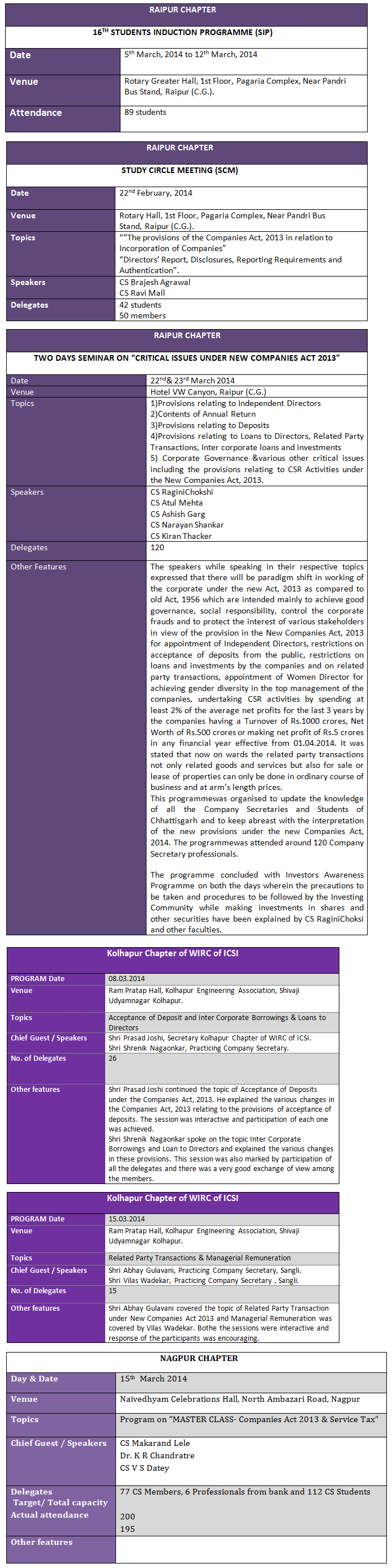

WIRC News

Chapter News

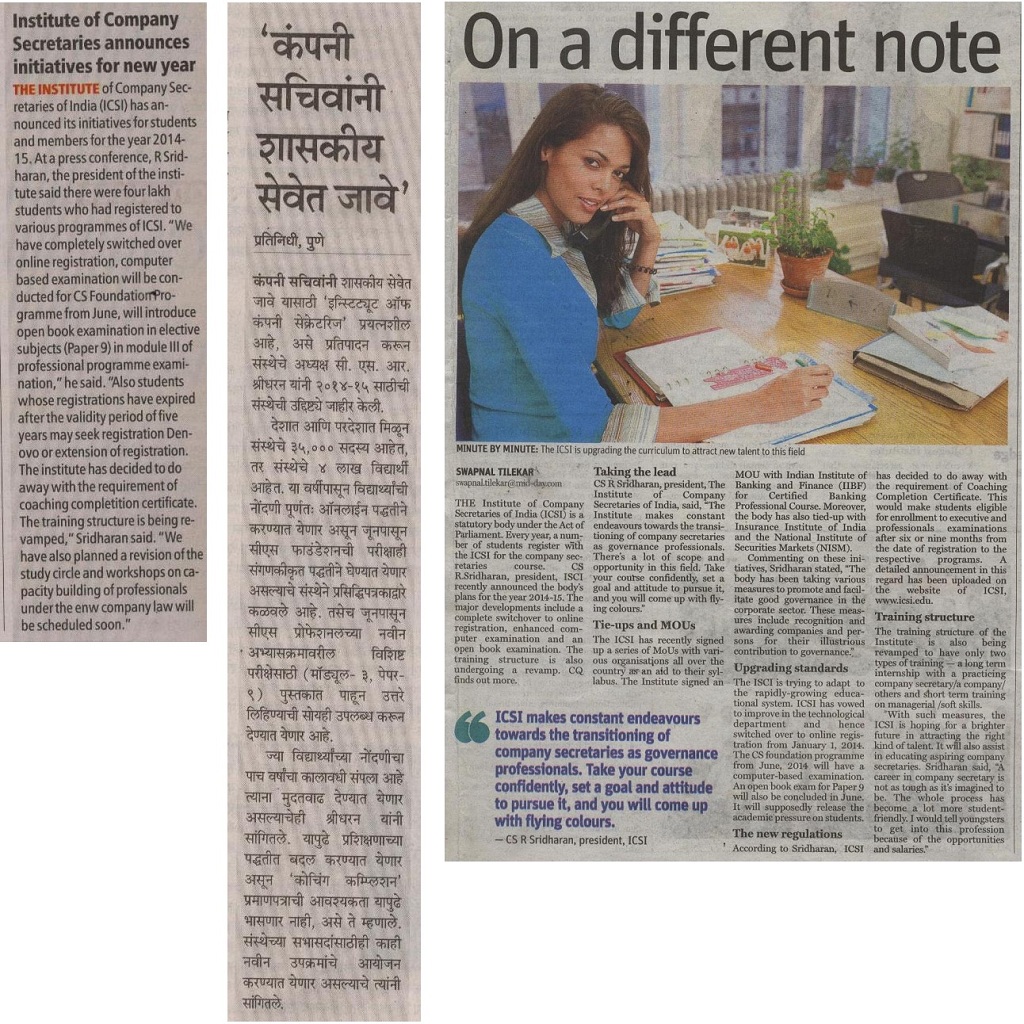

Media Coverage

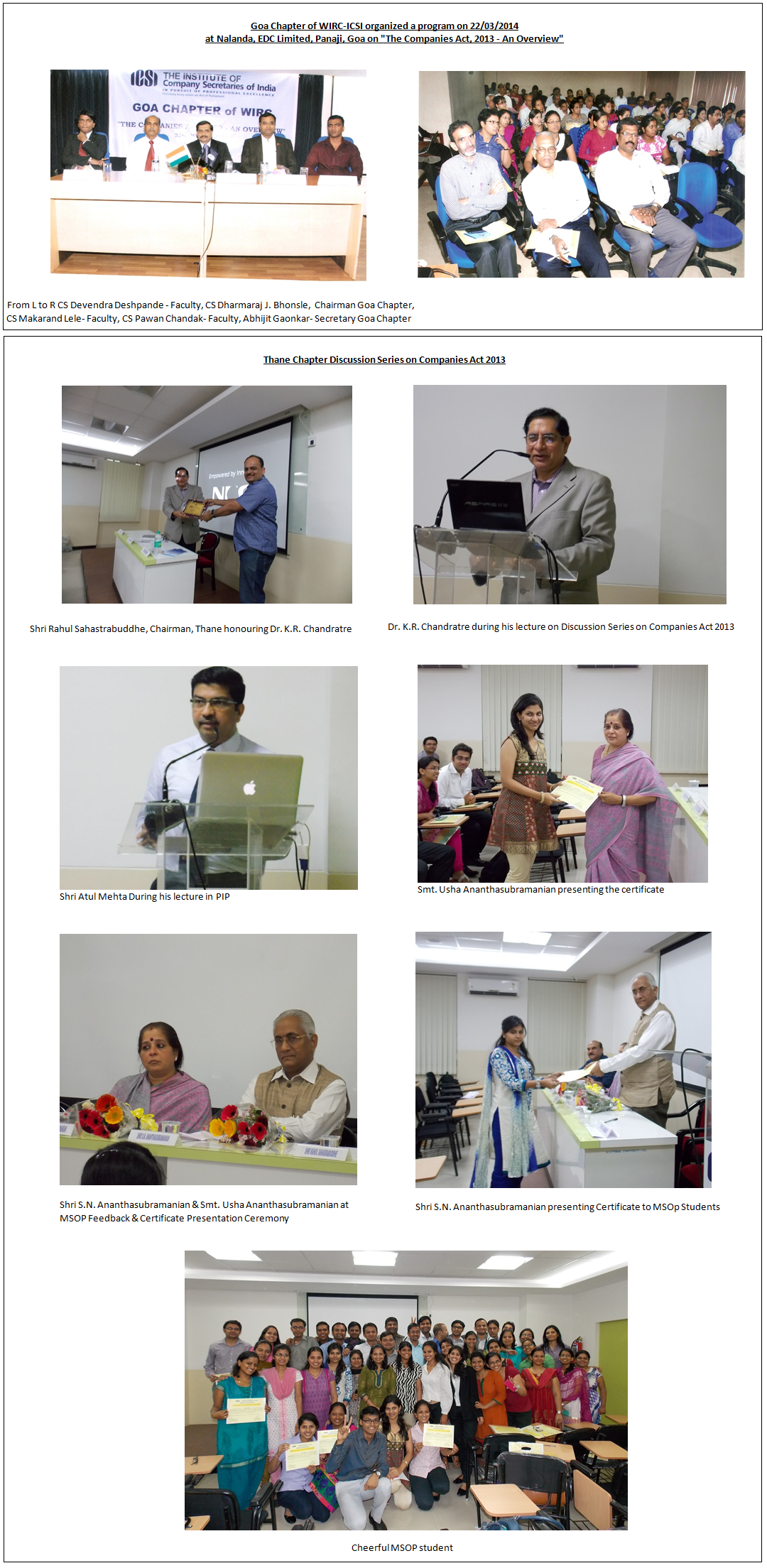

Chapter - Photo Gallery

WIRC - Photo Gallery

Editorial Policy

A : “FOCUS” published monthly as a magazine aims to be a forum for members of the Western India Regional Council of the Institute of Company Secretaries of India ( WIRC of ICSI) for;

a. DISSEMINATING information,

b. COMMUNICATING developments affecting the Institute and its members in particular and the CS profession in general,

c. ARTICULATING issues of contemporary concern to the members of the profession.

d. CEMENTING and DEVELOPING relationships across membership by promoting discussion and dialogue on professional issues.

e. DISCUSSING and DEBATING issues particularly of public interest, which could be served by the CS profession.

f. FACILITATING Members of the profession to share their views on matters of professional interest by way of articles and write-ups.

B : The WIRC of ICSI recognizes the fact that;

a. There is a growing emphasis on the globalization of the CS profession;

b. There is an imminent need to position the profession in a business context which transcends the traditional and specific CS applications.

c. The Institute members increasingly will work across the globle and in global context.

C : Given this background the WIRC of ICSI strongly encourage contributions from the following groups of professionals;

a. Members of other Professional bodies across the globe

b. Regulators and Government officials

c. Professionals from allied professions

d. Academia

e. Professionals from other disciplines whose views are of interest to the CS profession

f. Business leaders

D : The magazine also seeks to keep members updated on the activities of the Institute including events on the various practice areas

and the various professional development programs on the anvil.

E : The WIRC of ICSI while encouraging stakeholders as in Section C to Contribute to the Magazine , it makes it clear that responsibility

for authenticity of the contents or opinions expressed in any material published in the Magazine is solely of its author and the WIRC of ICSI,

council members, any of its editors or members of Editorial Team & Advisory Board, the staff working on it or “FOCUS” is in no way holds

responsibility there for. In respect of the advertisements, the advertisers are solely responsible for contents of such advertisements

and implications of the same.

F : Finally and most importantly WIRC of ICSI strongly believes that the magazine must play its part in motivating students to grow fast as

Members of tomorrow to be capable of serving the Legal & Compliance area within ever demanding customer expectations.

Tariff/Disclaimer